Happy New Year, have a successful year of 2024 ahead! Start with a big picture for 2024.

Biggest Trends Behind Biggest Deals in 2023

Two biggest trends – generative AI and climate tech — dominated the 10 biggest CVC deals in 2023 (from Global Corporate Venturing), the implications of these deals are in parentheses.

OpenAI, backed by Microsoft (AI is creating a new era)

GTA Semiconductor, China, backed by domestic investors (China chipmakers have big ambitions, although lagging far behind globally)

H2 Green Steels, backed by Hitachi Energy and Schaeffler (Big industrial processes are the next big growth area in cleantech)

Leapmotor, China, backed by Stellantis (China continues to create big EV startups)

Inflection AI, backed by Microsoft, Reid Hoffman, Bill Gates, Eric Schmidt, and Nvidia (Personal AI is going to be the most transformational tool of our lifetimes, that’s their bet)

Anthropic, backed by Amazon (Big tech companies are ready to make huge commitments to stake a position in the AI race)

Northvolt, backed by Volkswagen (securing batteries is crucial for automakers, other battery developers pulled in big money from carmakers – Verkor with Renault, China’s Libode New Material with GAC, Our Next Energy with BMW)

EnergyRe, backed by Novo Holdings (diversified investors have been attracted to climate tech, and energy transformation will speed up)

Redwood Materials, backed by Caterpillar Venture Capital and Microsoft’s Climate Innovation Fund (battery material recycling in the US is big)

Stack AV, backed by Softbank (betting big in the autonomous trucking startup risen from the ashes of Argo AI, Softbank’s still at the table)

Global ClimateTech Funding Held Up Well in 2023

Quoted from Crunchbase: “While 2023 has been a down year for startup investment in most industries, cleantech and sustainability-focused categories have held up comparatively well. Per Crunchbase data, global investors have poured approximately $13.9 billion this year into companies working on everything from battery recycling to water-conserving crops. That puts 2023 on track to come in roughly even with last year. The busiest cleantech investors were even more active in 2023, there is no sign they’ll pull back in 2024.”

Battery startups have the biggest investments, and companies to watch have an overlap with the previous top 10 CVC deals. Carbon removal and climate software have steady strong interests as well. From Pitchbook’s Q3 2023 Clean Energy Report, the grid infrastructure segment received the highest VC funding in Q3 2023, with 41.5% of the total deal value for the quarter. The biggest opportunity for energy transition lies in the biggest challenge – the infrastructure. We cover the new model of the Virtual Power Plant in this panel with Thomas and Bob.

Previously China led the world in energy transition investments, Europe as a whole is also ahead of the US, and now the US is catching up – “the IRA will pour around $1.2T into this space in 10 years, it’s not a cap, it’s a projection!” (Juan shared)

A big difference between the cleantech 1.0 era and now is that the capital stack for climate tech has been developed rapidly and much more mature in the past 5-7 years. The briefing for our panel with Paul and Karen on “ClimateTech Investor Panel – Capitalization and Financing” is a must-read. There is a massive flood of public funding or loans into the climate space, and investors with deep pockets for growth and physical assets are starting to raise and deploy investment vehicles earmarked for climate (Paul elaborated with examples). Furthermore, climate tech companies have gained a new exit path – private equity is emerging as a new opportunity for liquidity outside of traditional strategic acquirers – quoted from Kevin Stevens, Energize Capital. He noted: “This trend is set to continue in 2024. The one nuance is a newly added emphasis on profitability alongside growth as servicing debt costs remain high.”

Defence Tech is the Sector Winner of all in 2023

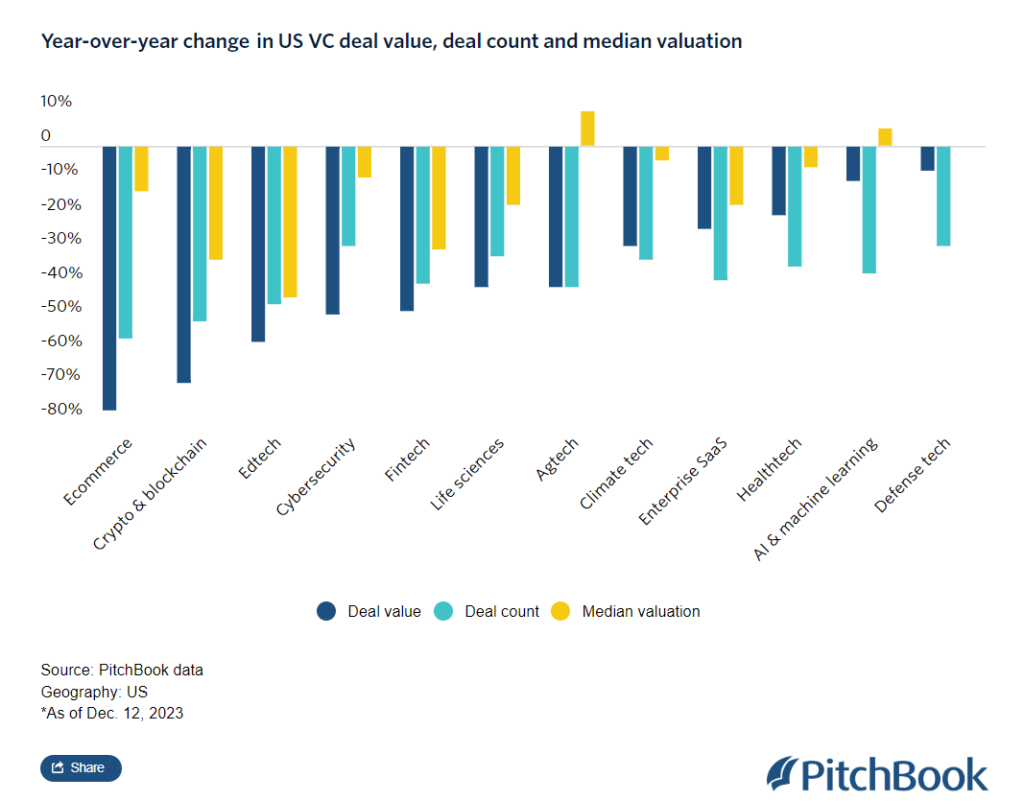

In this chart (below) from Pitchbook looking at sectors in terms of deal value, counts, and median valuation, we might notice AgTech’s median valuation jumped 10% YOY, AI/ML’s median valuation increased by 5% YOY, climate tech’s valuation also held up better than others, but Defence tech has the minimum decrease in deal value and counts. National security became a concern amid the technological arms race with China and wars in Ukraine and Israel.

The success of companies such as Anduril and Palantir showed investors that a more significant portion of the Pentagon’s growing budget could be captured by VC-backed startups rather than traditional defense contractors such as Lockheed Martin and Raytheon. US President Joe Biden has just signed the $841bn Defense Spending Bill for FY24, with an added focus on research and prototyping in areas such as missile defenses, hypersonics, space domain, etc.

US-based companies in the category collected nearly $100 billion in VC funding from 2021 to now, a figure that’s about 40% higher than what was invested in the seven prior years combined, according to PitchBook data. (Go deeper: 2023 Vertical Snapshot: Defense Tech) And New York Times has identified at least two dozen venture capital, government contractor financing or private equity firms that are run by or have hired former Pentagon officials or retired military officers, with most of the hires having taken place in the last five years.

A Profound Reset of the VC Industry

Quoted from the CEO of Techstars: “What the VC industry is currently going through is not cyclical, but a profound and unprecedented reset.Nothing in the data, or anecdotally in my own conversations with LPs, VCs, our corporate partners and Techstars portfolio companies suggests that a rapid V-shaped bounce-back is on the horizon…. rather than a prelude to a recovery, 2024 will be much more of the same. Her predictions for the VC industry in 2024: (Read the whole letter here)

1 – U.S. family offices will increasingly invest directly in startups. 😎

2 – There will be fewer VCs and unicorns. 😉

3 – Regulatory complexity will become a thing for VCs. 🤔

4 – The best accelerators will become more pertinent. 🤗

5 – Alternative venture models will come to the fore.” 😶

Lots of data indicated that small funds have better performance than large funds, but smaller funds will struggle more to raise funding in this climate. And, the unit economics of small/micro VCs is challenging to cover all aspects needed. New models might be emerging.

Global League

This is Jessie Chuang with Global League – a vetted network for professional or accredited investors to identify the most impactful ventures for impact investing.

We’ll resume ClimateTech Investor Panels in January 2024, and look forward to highlights on top investment opportunities. Recommendations on speakers – investors, experts, or startups – are welcome. Here are January’s topics:

Sustainability of Built Environment (Jan 12)

Sustainability of Food Supply Chain (Jan 19)

Sustainability of Water and Ocean Tech (Jan 26)

Green buildings startups are buckling the trend with $5.3B raised in 2023, on track for their best year ever and marking a threefold increase from 2020. (from Urban Tech report by 2150 x Dealroom) We will cover this in the next newsletter.

The IRA allocated around $400 billion in federal dollars for clean energy projects. It aims to incentivize the manufacturing or projects of clean energy in the US through multiple tax credits, targeted mostly toward solar and wind operations.

The Advanced Manufacturing Production Credit (AMPC) affords manufacturers tax credits for producing qualifying devices needed for clean energy projects. The amount of the credit is determined by the device, its specific function and its capacity.

The Production Tax Credit (PTC) grants tax credits to wind projects up to 2.6 cents/kWh of energy that they produce.

The Investment Tax Credit (ITC) incentivizes solar energy companies to further invest in their U.S.-based operations by offering up to a 30% tax credit on “energy property,” a definition that has been newly broadened with this act.

The PTC and ITC tax credits do come with some fine print, such as a three-year window in which companies must begin construction to qualify. There are also prevailing wage and apprenticeship requirements that determine whether companies qualify for all the aforementioned rates or just 20%. These tax credits serve as massive incentives for companies to expand their operations in the U.S. The IRA also encourages households and individuals to invest in clean energy products through tax breaks.

A little more than one year after the passage of the IRA, what has happened to the clean tech landscape? Manufacturing dominates the major theme. (reference)

There’s a battery boom across the country—the IRA tax credits available are projected to cut the total cost of U.S.-manufactured battery cells and packs by one-third. 91 companies have announced new battery projects totaling $77.7 billion in investments.

Eight of 25 new projects in clean tech are in semiconductor manufacturing. The others range from sustainable aviation fuel to manufacturing tools for home energy efficiency. All together totaling in 133.38 billion invested.

About 65 new electric vehicle projects totaling 44.1 billion in Domestic EV production investments were announced.

Private investments might surpass the public funding, in one year more than 270 new clean energy projects with private investment totaling $132 billion were announced according to an August report from Bank of America Global Research. More than half of them went to EVs and batteries, the rest went to renewable energy, grid storage, carbon capture, utilization and storage and clean fuels. BoA expects these investments to create more than 86,000 jobs, including 50,000 in EVs.

Capital from the IRA will mostly flow toward established companies, but private investment, like venture capital, is finding its way to startups across all stages. Many startups have cropped up to offer auxiliary services to larger industries. The number of startups has risen significantly, including solar, stationary, and long-duration energy storage, energy transmission, hydrogen energy, carbon capture and sequestration, domestic EV manufacturing, and EV charging.

American companies restored almost 350,000 manufacturing jobs in 2022 — a 25 percent increase from 2021. If looking back on a one-year timeline from August 2022 to August 2023, the manufacturing sector job growth number is around 123,000. (reference)

Besides IRA, the CHIPS Act supports a domestic semiconductor supply chain for the U.S. Clean energy manufacturing, such as solar panels, wind turbines, and electric vehicles (EVs), is heavily dependent on semiconductor chips at the core. Even this $1B plant – New-Zero 1 – aimed to turn corn into jet fuel using wind and solar energy needs semiconductor devices. Now US semiconductor is booming synergetically to spring the unprecedented clean energy sector expansion.

Transistors, such as IGBTs and SiC MOSFETs, play a critical role in perhaps the most important device within all these machines: the inverter. Wind and solar inverters convert DC energy into AC energy (AC) to allow the electricity to be distributed through the grid into homes and facilities. In EVs, the inverter plays the same role, turning the DC energy from the car battery into AC energy used to power the car’s various electronic components. Those wind and solar inverters are qualifying AMPC devices to receive tax credits to reduce the overall manufacturing cost. Along with transistors, another type of semiconductor that could see higher demand is multilayer ceramic capacitors (MLCC). A significant portion of MLCC demand is driven by the automotive industry, specifically as it pertains to EVs. A single EV can contain up to 18,000 MLCCs, and as EVs become more sophisticated, that number is expected to grow rapidly.

These are just a few examples. In general, semiconductor manufacturing is a national security priority now, especially owning/onshoring advanced semiconductor manufacturing capability. One Year after the CHIPS and Science Act, the White House marks historic progress – Companies have announced $166B in investments in semiconductors and electronics on top of $52.7B promised by the Act. The report also summarizes actions supporting regional economic development, investing in innovation, building jobs, and workforce pipeline in semiconductor manufacturing. As AL/ML is integrated into more verticals, the race for computing speed, power, and efficiency as well as emission reduction is driving the advanced semiconductor frontier innovations in the US. Microchips that can handle AI workloads are in high demand for data centers, autonomous vehicles, inferencing at the edge, and more. Semiconductor is an enabler and technology multiplier to all. It drives a whole supply chain economics and its high barrier drives advancements in many technologies. Open innovation strategy is common in this industry.

Manufacturing presents a huge opportunity for applied machine learning. It’s a massive space — north of $5 trillion in the US alone — and increasingly data-rich. Manufacturing investments might be too capital-heavy that small VCs and angel investors can’t participate in, but the ecosystem is huge. Capital-light value providers from design support, metrology, new materials, sustainability, digitalization, optimization, and automation for manufacturing factories, and even workforce development could be opportunities for small private investors. However, the knowledge barrier is very high.

Join Global League to learn about potential investment opportunities in these.

Startup funding is shifting from generative applications to infrastructure solutions to support enterprises build internal tools

Language use cases dominate enterprise spending and VC investment

Emerging AI startups with short-term tractions are everywhere, investors need to understand their defensibility and profitability

Generative AI’s fast emerging market

The global generative AI market is expected to reach $42.6 billion in 2023. This sector is the top trend observed from where recent VC funding goes.

The early stage of a tech stack is emerging in generative AI. Hundreds of new startups are rushing into the market to develop foundation models, AI-native apps, and infrastructure & tooling. Models like Stable Diffusion and ChatGPT are setting historical records for user growth, and several applications have reached $100 million of annualized revenue less than a year after launch.

What has now become the critical question: Where in this market will value accrue? Where do VCs bet on? Take a quick look at the sub-sectors with bigger funding: (> $500M in total)

Investment in infrastructure solutions stands out

AI development infrastructure:

AI applications creation and productionization, e.g. AnyScale

Run, tune, and deploy generative AI models on any hardware or in the cloud, e.g. OctoML

Vector database for vendor search, to power semantic search, recommenders, and other applications that rely on relevant information retrieval., e.g. Pinecone

AI data labeling, curation, and model integration:

Automated data labeling, integrated model training and analysis, and enhanced domain expert collaboration, e.g. Snorkel

Generative AI architecture to integrate foundation models and all models, full stack for enterprise AI, e.g. Scale AI

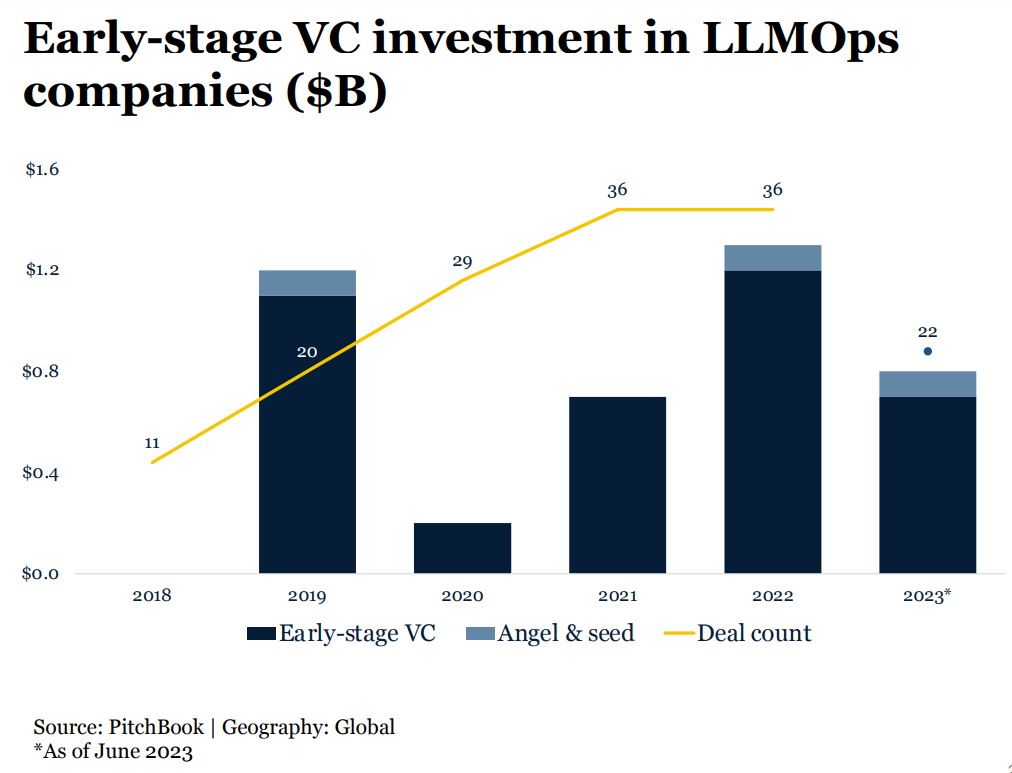

In the following chart from Pitchbook, the trend of early-stage VC investment in infrastructure solutions and data platforms going up is very strong against the backdrop of the overall financing climate downturn.

Breaking down the funding flowing into different capabilities in LLM infrastructure shows a lot of new startup categories are forming, including vector databases, prompt engineering, LLM model architecture, LLM orchestration, and LLM deployment, though winners are not yet clear.

Talking about AI infrastructure, everyone knows AI chips underlie all AI computing, but semiconductor is an area with a higher barrier of knowledge and resources for most VCs (read more about semiconductor AI opportunity here), investing in the software stack layer makes sense for them. It’s also a long-term bet, but without starting investing investors don’t get the learning opportunities toward a 10x return.

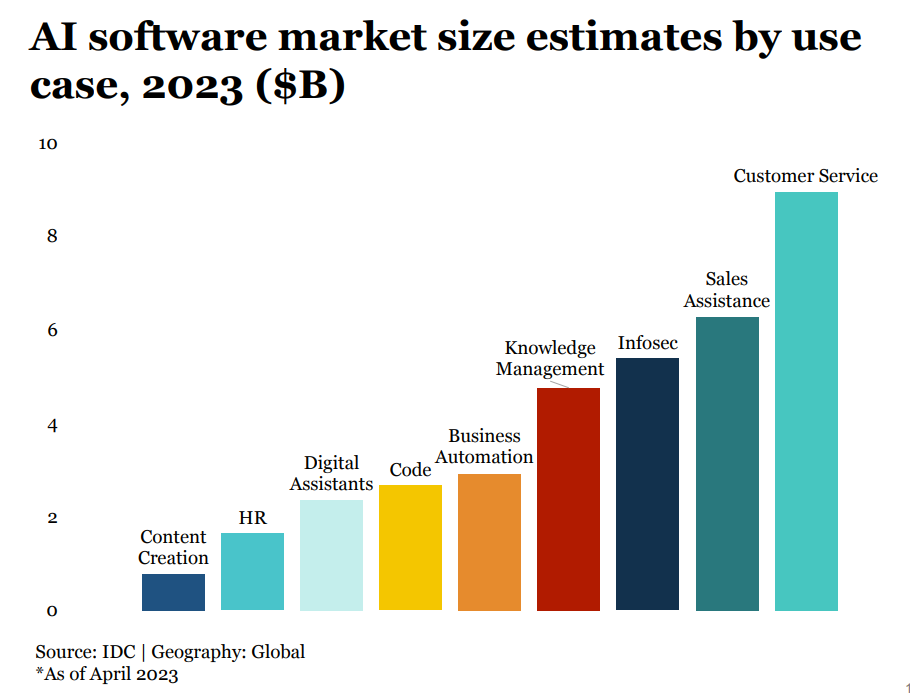

Language use cases are the new focus in AI applications

Language use cases dominate enterprise spending and VC investment. Applications in sub-sectors like marketing and sales assistance, customer service, infosec, and knowledge management get higher funding.

Visual media and content creation:

Content creation suite for marketing or the like, e.g. Jasper (B2B or B2C content creation tool without proprietary models)

Video creation tool, e.g. Synthesia (it makes video production possible for companies without actors, cameras or studios.)

Audio:

Summarization for meetings, e.g. Fireflies.ai

Coding:

AI coding assistants, e.g. Kodezi

Natural language interface:

Chatbot and assistants (interface with customers), e.g. PolyAI, Cresta

Search and knowledge discovery, e.g. Glean

Investors seeking long-term winners

In 2023 January, a16z wrote:

The growth of generative AI applications has been staggering, propelled by sheer novelty and a plethora of use cases. In fact, we’re aware of at least three product categories that have already exceeded $100 million of annualized revenue: image generation, copywriting, and code writing.

However, growth alone is not enough to build durable software companies. Critically, growth must be profitable — in the sense that users and customers generate profits (high gross margins) and stick around for a long time (high retention). In the absence of strong technical differentiation, B2B and B2C apps drive long-term customer value through network effects, holding onto data, or building increasingly complex workflows.

In generative AI, those assumptions don’t necessarily hold true, since the technology itself might change the market dynamics. (read more here)

All moats on deck

Getting OpenAI to focus on a particular corpus and answer questions from that corpus is no longer hard for people with a background in building software solutions. Open-source resources are available to startups as well as incumbents. Emerging AI startups with short-term tractions are everywhere, investors need to understand their defensibility and profitability in either vertical or horizontal positioning. Due diligence and analysis in technology, business, and other kinds of moats are important.

Investors can ask the startup what LLMs they’re using, whether and how they’re fine-tuning, and what their plans are for developing in-house models. Vertical LLMs might replace horizontal LLMs. Insights and data in verticals are a strong moat. Also, investors can ask how well/fast their solutions are adopted by their target audience. User experience and real impact metrics must be delivered, for example, productivity enhancements, and error rate reduction. Even a 1% improvement times a huge business value is worth pursuing.

AI transformation in many verticals is exciting, some verticals might see faster changes than others. But those investors who pursue only fast growth might miss long-term profitability. Behavior change, trust from users, organization change management (workflow change, value chain change…), regulations, physical limitations, relationship building, and other factors might create friction for AI adoption, but overcoming a barrier might become a moat that sticks for long. Last but not least, investors and startups need to watch the market landscape to prevent working on something that tech giants might come in later and take it away.

VC investors have already shifted their focus to categories in which startups can carve out AI chip market share. In 2021 and 2022, AI/ML VC deal value in inferencing has become significantly larger than training-focused only, breaking a historical trend.

Both the PC and automotive AI chip markets are growing faster than the data center AI chip market at over 30% each, at this pace they will surpass data center’s market size by 2025.

Edge inferencing is likely to be dominated by existing vendors, all of which are investing heavily in supporting transformers and LLMs. So, what opportunities exist for new entrants? Automotive partnerships could be the hope; second, supplying IP or chiplets to one of the SoC vendors; and, creating customized chips for intelligent edge devices that can afford the cost.

PC and automotive AI chip markets

AI computing remains a major growth driver for the semiconductor industry, and at $43.6 billion in 2022, the market remains large enough to support large private companies. Also, the AI semiconductor market is divided into companies in China and those outside of China, because of the current political circumstance.

Nvidia is clearly the leader in the market for training chips, but that only makes up about 10% to 20% of the demand for AI chips. Inference chips interpret trained models and respond to user queries. This segment is much bigger, and quite fragmented, not even Nvidia has a lock on this market. Techspot estimates that the market for AI silicon will comprise about 15% for training, 45% for data center inference, and 40% for edge inference. The serviceable market for foundation model training will likely remain too small to support large companies, thereby relatively low acquisition offers are possible. Where is the opportunity?

Data center, automotive, and PC, these three sectors take 90% of the AI chip market if excluding the market of smartphones and smartwatches (to prevent data bias from Apple and Samsung), but the data center has 6 vendors taking 99% of market share, that market is saturated.

Both the PC and automotive AI semiconductor markets are growing faster than the data center AI semiconductor market at over 30% each, at this pace they will surpass data center’s market size by 2025.

Inferencing at the Edge

In the past 2 years, we saw a 69.0% decline in year-over-year VC funding for AI chip startups outside of China, VC investors have already shifted their focus to categories in which startups can carve out market share. In 2021 and 2022, AI/ML VC deal value in inferencing has become significantly larger than training-focused only, breaking a historical trend. Also, edge computing demands are driving more commercial partnerships for inference-focused chips than for cloud training chips.

Custom chips and startups can outperform the chip giant on specific inference tasks that will become crucial as large language models are rolled out from cloud data centers to customer environments – Inferencing at the Edge. The term ‘edge’ is referring to any device in the hands of an end-user (phones, PCs, cameras, robots, industrial systems, and cars). These chips are likely to be bundled into a System on a Chip (SoC) that executes all the functions of those devices.

What opportunities exist for new entrants?

Edge inferencing is likely to be dominated by existing vendors of traditional silicon, all of which are investing heavily in supporting transformers and LLMs. So, what opportunities exist for new entrants?

Supply IP or chiplets to one of the SoC vendors. This approach has the advantage of relatively low capital requirements; let your customer handle payments to TSMC. There is a plethora of customers aiming to build SoCs.

Find some new edge devices that could benefit from a tailored solution. Shift focus from phones and laptops to cameras, robots, drones, industrial systems, etc. But some of these devices are extremely cheap and thus cannot accommodate chips with high ASPs. A few years ago, many pitches for companies looking to do low-power AI on cameras and drones. Very few have survived. But, edge computing has become more prevalent in the trend of “smart everything”, and computing platforms also extend into wearables such as Mixed Reality headsets, technology advancements always push new possibilities.

Automotive partnerships could be the hope, this market is still highly fragmented, but the opportunity is substantial. In Q2 2022, edge AI chip startup Hailo announced a partnership with leading automotive chipmaker Renesas for self-driving applications.

As the world is going through a major trend of electrification for decarbonization and automating optimization of energy usage and everything, edge AI chips with the right upstream and downstream partnerships are promising opportunities for investors and startups. The financial downturn may encourage M&A for some startups that align with the product needs of incumbents. Some historical examples are Annapurna Labs’ $370.0 million exit to Amazon and Habana Labs’ $1.7 billion exit to Intel.

Climate Tech Circle Time with Noah Miller, Founder & Chief Strategist, Rho Impact on 2022/11/23 at 9 AM CT

Our society desperately needs investments to reverse climate change, but there is no objective evaluation mechanism when undertaking due diligence with investment targets. Quantifying sustainability impact is critical for investors to better identify, evaluate, and communicate the technologies that will reduce emissions.

In this session, Jessie invited Noah of Rho Impact to discuss how they help Eclipse Ventures build up a framework for assessing the potential climate impact their portfolio could make, and share his observations on the recent developments from COP27, the Biden administration’s proposed plan to protect the federal supply chain from climate-related risks, and more from the landscape.

Many greenwashing scandals and lawsuits show that lack of validation of ESG claims has been a serious issue; ESG disclosure regulations in major markets (US, EU, China) are influencing decisions in B2B customer acquisition and investment capital.

ESG disclosures inform everything from ESG raters to institutional investors/advisors to lists of the best ESG products for consumers. The implications in reputational, operational, and financial consequences for enterprises are significant in terms of investor and customer acquisitions, due diligence for M&A, loan applications, and insurance.

Because of Scope 3 commitments from major brand names, their suppliers must be able to provide and validate ESG data to do business with them. US Supplier Climate Risk Rule also requires suppliers report Scope 1, 2, 3 emissions, climate risk assessment alignment with TCFD (Task Force on Climate-Related Financial Disclosures), and emission reduction targets validated by SBTi (Science Based Targets Initiative).

COP27 has reached the “Loss and Damage Fund” deal. Explosive funding will be deployed to climate tech verticals – carbon capture, emission reduction, climate adaption resilience, sustainable food system, etc. at a global range. Especially there is a major focus and market opportunity in food tech.

An important reflection from COP27 is the lack of stakeholder engagement from all countries. In order to get broad acceptance, commitment, and deeper collaboration from all stakeholders, the process needs to be equitable as well as the outcomes.

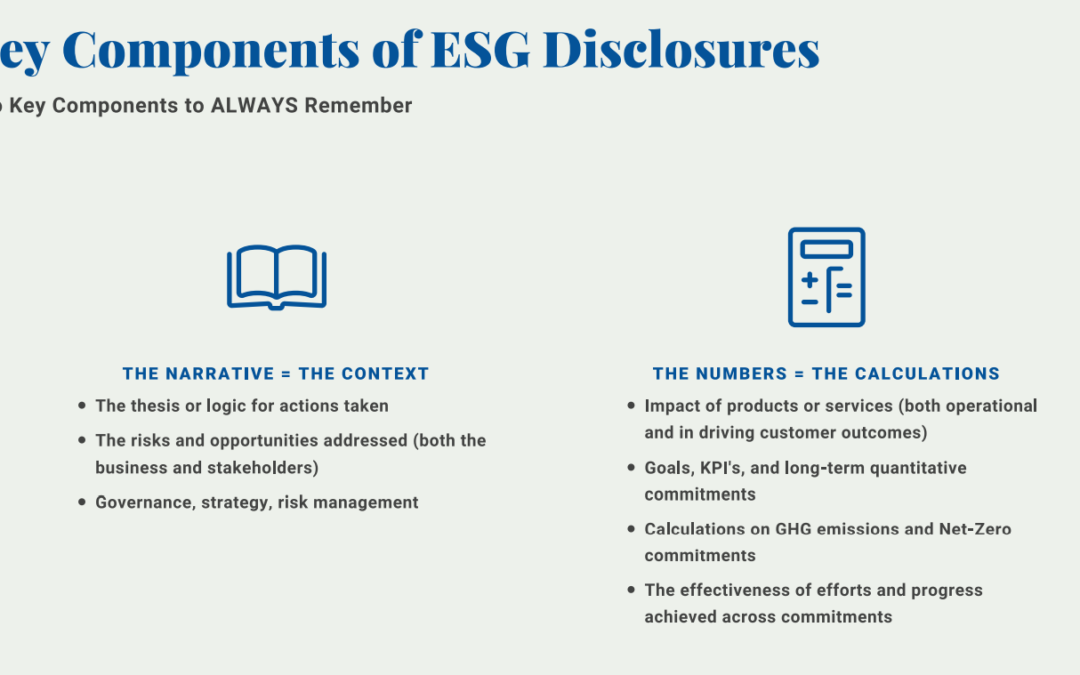

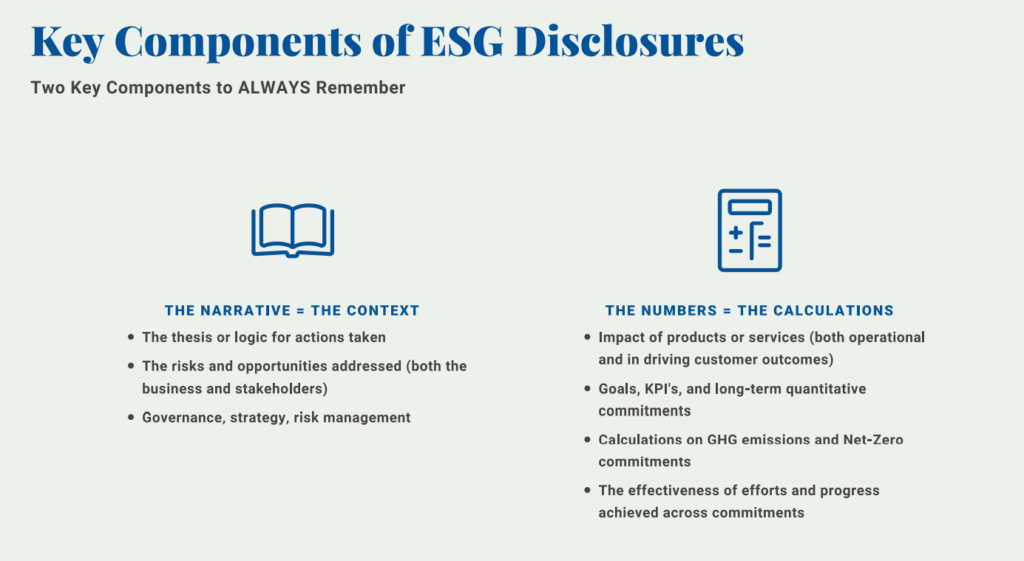

Key components of ESG disclosures include the narrative (the context including the thesis or logic of why you are doing what you are doing, the risk and opportunity you are addressing, the governance structure for overseeing the work, the overall strategy of business model and driving performance, how you are managing associated risk that might come with the work) and the numbers (the calculations). Some emerging de facto standards are informing a lot of rating/ranking systems and disclosure regulations (signs of unifying standards), but the emphasis of baseline comprehension – the narrative – from a buyer or investor standpoint is going to increase in parallel. 3rd party validation and certification for ESG reporting is an effective model to prove all boxes are checked for both the deeper context and the calculations.

In the voluntary carbon market, carbon offsets exchange is a great tool for financing carbon reduction projects; it will be a trillion-dollar market. We will see more standardized methods for verifying, monitoring, and certifications to improve accountability, but a global standardized carbon market is still far away and local initiatives will continue to take off.

The carbon accounting software market is too crowded; there will be consolidation events in the coming year. Commodity-like software alone isn’t enough as realities are too complicated. Most organizations like to have bespoke software as well as humans in charge of action planning/execution.

In terms of the cost of ESG certifications being a burden for suppliers, there are many free ESG project management tools and resources out there. Any companies working with facilities and materials should at least start tracking metrics and issues to build what’s needed to bid for customers; they will benefit from energy savings with all the data and insights built up even before the benefits of acquiring customers.

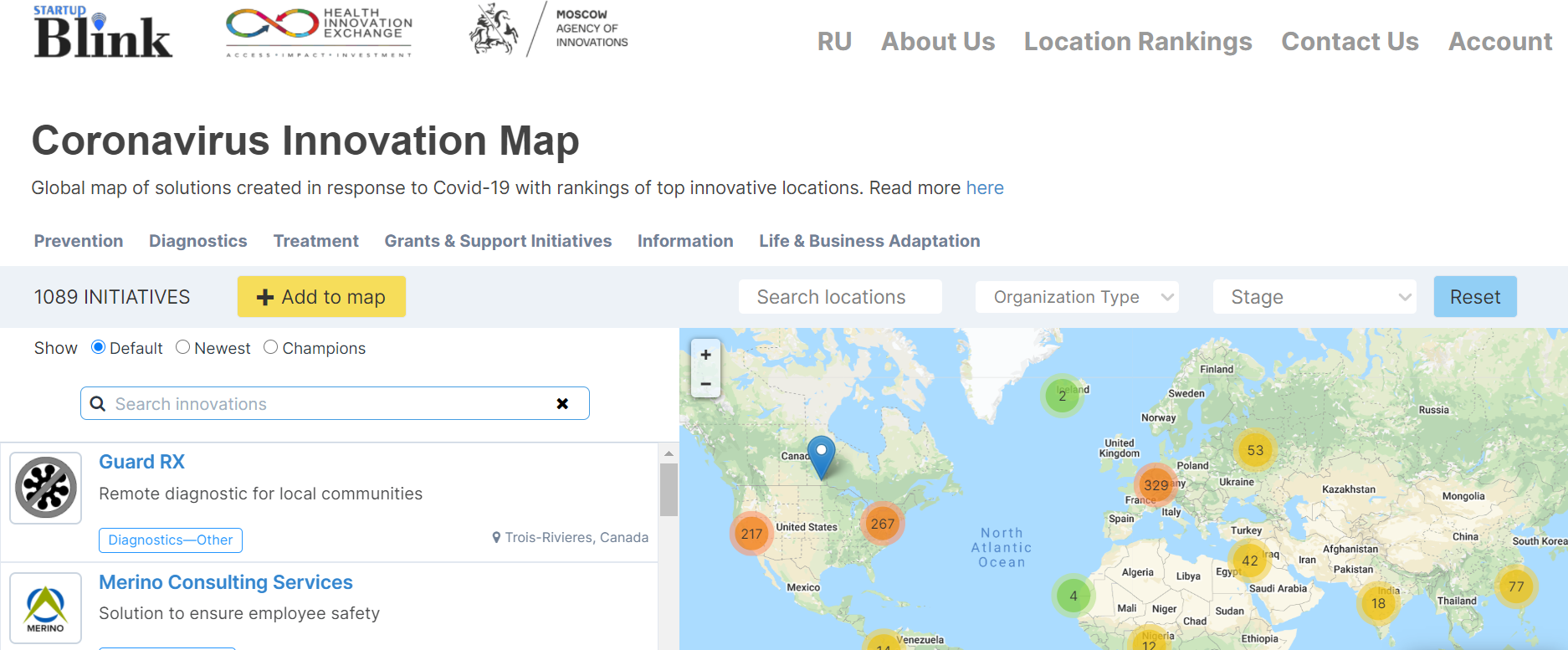

Coronavirus Innovation Map is a platform of hundreds of innovations and solutions from around the world that help people cope and adapt to life amid the coronavirus pandemic, and to connect innovators.

The CoronaVirus Innovation Map is a visualized global database that is mapping the innovations related to tackling coronavirus in various fields such as diagnostics, treatment, lifestyle changes, etc., on a geographical scale. Listings are added by the research teams of StartupBlink and the partners, as well as crowdsourced by the global community. In fact, anyone can suggest an initiative to be added!

StartupBlink has innovative proprietary technology databases and algorithms that we use to map startup ecosystems and innovation. This puts us in a position to produce customized databases depending on the type of innovation at hand. The technology required is ready and since COVID-19 has sparked a lot of innovation because of its novel status, StartupBlink is able to gather more data about this innovation and reflect it on our database that is already being used as a resource for startup ecosystem innovation.

We are glad to have a brief interview with StartupBlink CEO Eli David to get his high-level observation on the innovation landscape in 2020.

Q1 : What are the major changes in startup ecosystems in 2020?

The major changes in the startup ecosystem in 2020 is, of course, the digitalization. And anything that can provide the solution in a way that does not involve humans is become very, very attractive compared to others.

Q2 : Among these changes, what do you expect will have a lasting impact after COVID-19?

Let’s say startups that have to do with the more physical ecosystem like tourism, aviation, are definitely received quite a hit. So, there are clear winners in 2020 compared to also clear losers as well. Also a lot of startups that were not so relevant, are disappearing. So, 2020 is not a major crisis here. It’s just a year of change, in a very, very deep change.

The lasting impact after COVID-19, the digital world anything that has to do with online experiences is going to receive more attention from people. I think remote work is going to be have a very lasting impact. Now that culturally, it is allowed to think in remote work, there’s going to be a lot of impacts.

Q3: Regarding technology and innovation developments, what is accelerated, and what is slowing down in 2020?

Actually, the online world is going to receive a lot more of our attention and budget compared to the offline world. Basically, the entire world is moving online. So, anything that can accelerate that is very successful, and anything that has to do with the physical world has been slowed down massively and suffered the most, we all know them.

Q4: Do you see startups/small businesses adopt more automation on AI solutions to enhance their productivity and agility?

Yeah, I think startups will definitely adopt more AI solutions. However, the problem is that, for small businesses, they have a problem to adopt AI because AI is usually very expensive. So, I have a feeling there’s going to be more than anything. The corporate and AI is going to help the corporate even get more market share. And the startups themselves are going to try to develop something unique and then sell it to the corporate just like always. But there is a limit over here, that the bigger companies, the more it has advantages and relatively small startups cannot really compete with them and that’s always a problem. But it’s more than anything a problem right now.

Q5: What do startups or scale-ups need the most from startup ecosystem builders in 2020?

The startup ecosystem builders in 2020 have to be active. They have to help ecosystems, they have to be more than anything to work on the infrastructure of the ecosystems, and help startups and founders fulfill their potential. And we’re talking more than anything about removing red tape, bureaucracy, and also promoting direct systems to make sure that people know about their ecosystems, because ecosystems basically are competing for talent, and that’s always important.

Q6: What are those startup ecosystems builders that have done an impressive job to support startups this year? (1~3 examples on top of your mind)

I think the ones that have done really good work, I have a few examples. I like the examples of the relatively smaller location. And one that comes to mind is Kingston in Canada. It’s a relatively small city, close to the bigger cities in Canada, but still managing to differentiate and be successful and those are exactly the examples we’d like to see. Kingston is working heavily with the good universities in Kingston, mainly Queen’s University. And they’re managing to do a very impressive job in attracting people from outside of Kingston and also keeping their own local talent without leaving.

The same is happening in the Sunshine Coast in Australia, another example of a relatively small city. These very, very active on the promotion of the tech system and the development. I think it’s another nice example of how a relatively smaller city can be very successful in promoting and enhancing their ecosystem.

One more example would probably be the municipality or the chambers of commerce in Cali in Colombia, they’re also doing a great job to compete with a bigger city and create creative regional hubs. So, it’s always nice to see the quality of the work from the ecosystem developers of the smaller locations.

Q7: What are those startups that have done an impressive job to pivot and innovate this year? (1~3 examples on top of your mind)

As for the startups, I have to say that I can’t really think about specific examples, but I will tell you that the startups that I like seeing the most are the ones that have pivoted this year, instead of waiting for a normal life to come back, the startups actually leveraged on this crisis, change their business model, and are very, very flexible.

And I think a few examples can show that. The biggest one is probably is Zoom and Peloton, and companies that have seen the demand for the products really increase and keep on customizing it based on a new reality. We have a COVID-19 map at coronavirus.startupblink.com built together with United Nations that actually features more than 1000 startups that are innovating. There is so many, many startups are innovating on prevention and diagnostics, so it’s absolutely great to see.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.