Augmented reality (AR) is technology that blends digital content with the real world. It is often referred to in conjunction with virtual reality (VR), which completely replaces the real world with a digital one. Through cameras and sensors, an AR device can locate objects and gather information to model the physical environment in real time. Then, algorithms process this data and overlay digital elements onto the surrounding area.

When hearing the words “augmented reality,” people often think of Niantic’s outrageously popular 2016 mobile game, Pokémon Go. But although the capabilities of Pokémon Go were captivating enough four years ago, AR technology is continuing to improve even further thanks to innovative companies like Microsoft, Zappar, and Magic Leap.

For example, one of the best uses for AR currently being developed is remote collaboration. AR systems can achieve “natural face-to-face communication” along with digital interactivity, combining the benefits of in-person and virtual teamwork. From miles away, one person could work simultaneously with another in a digital 3D workspace, sharing information or making changes.

In the past two to three years, another important development has been the enabling of no-code authoring. This feature allows non-developers, including students, to create content for AR applications, thus significantly reducing its adoption barrier and increasing its accessibility to the public.

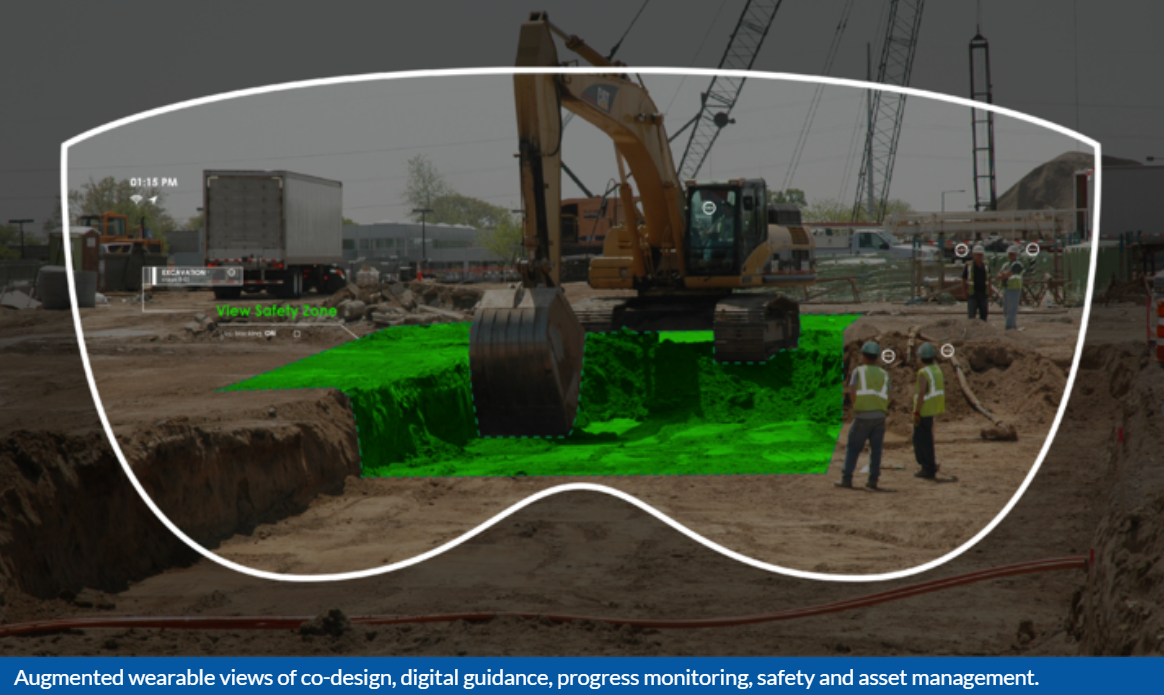

The increasing value of AR has made it attractive to multiple different sectors. As Pokémon Go and other applications demonstrate, arts and entertainment sectors have already benefited from the use of augmented reality to enhance user experience. Another industry that is taking advantage is design and architecture. Tools like Morpholio AR Sketchwalk and DAQRI Worksense facilitate more efficient construction with 3D modeling, hands-free viewing of schematics and/or instructions, attaching data to real objects for future reference, and other features. Manufacturing operations are advanced by AR in the same ways, minimizing error and reducing the time and effort required.

Image from: Advanced Manufacturing Research Center (amrc.co.uk)

The retail industry is another field that can profit greatly from the use of AR devices. Shoppers looking for clothes, furniture, or other objects would relish the opportunity to check out how those items would look in real life. Companies like Vyking and Wayfair have already created applications that let customers visualize their products over themselves or their surroundings.

In the healthcare industry, workers are employing AR to conveniently show crucial patient data during operations, allow doctors or surgeons to work together though physically distanced, or help explain medical situations to patients. Additionally, augmented reality could facilitate more effective education by placing students into realistic training simulations or providing useful supplementary materials for them to use. Organizations can implement AR into reskilling/upskilling employee training programs, thus allowing workers to quickly become more flexible and experienced. Regardless of the subject being studied, AR can offer a more hands-on experience that encourages students to be more active in learning.

Overall, augmented reality could also drastically transform a typical workplace environment. Workers could communicate remotely with experts or coworkers, easily use digital features to assist with their duties like measurement tools, and access needed information without having to pause their tasks. In the future, computers and physical offices could be totally replaced by much smaller AR devices for every employee. Especially when combined with other advanced technologies, such as 5G or artificial intelligence, the rise of augmented reality could lead to huge changes in how people work and learn.

Given the unique potential of this technology and the progress it has already made, investors and businesses should keep a close eye on the AR market. Though it may still take some time for AR to become powerful and accessible enough to reach wider markets, there is no doubt that it will transform several industries over the next few years.

“Venture firms became much more conservative around dealmaking as the pandemic hit the US in March and early April, leading to a downturn in both VC invested and number of deals completed in Q2. Portfolio companies followed suit, adopting an understandably cautious outlook as they sought to reduce their burn rate through layoffs, cost-cutting, and curtailed expansion plans.”

“But, the impact on aggregate VC activity was hardly apocalyptic. Much of the slowdown occurred during the early part of the quarter, when uncertainty over COVID19’s impact on the economy was at its height. After the initial month and a half of exercising caution, triaging, and focusing primarily on stabilizing their own portfolio companies, VC investing began to pick up in May. While some sectors have been heavily affected by the pandemic, many startups, especially in the software and biotech sectors, have fared relatively well during the COVID-19 crisis, offering solutions to the healthcare, digital enterprise, and consumer services needs of the country.”

“Valuations have not dwindled as much as many industry professionals expected, and the ample dry powder in the industry has allowed VCs to continue making investments—even large ones—during the second quarter.”

“The VC industry is on pace for a record number of mega-deals, while first-time fundings are tracking for their lowest annual total in 10 years. That’s a sign that LPs are opting to commit their capital to established managers with track records of success rather than the many upstarts that made a splash the past few years.”

“The result has been a surprising fundraising boom amid an otherwise turbulent market. Firms closed $42.7 billion worth of venture vehicles in the first half of 2020, by itself a higher sum than all but three of the past 15 full years.“

“This explosion of outsized funds drove the 2020 median fund size back over $100 million for the first time since 2007. Led by major efforts from firms such as General Catalyst, Lightspeed and DCM, the median and average VC fund sizes have both more than doubled compared to 2019.”

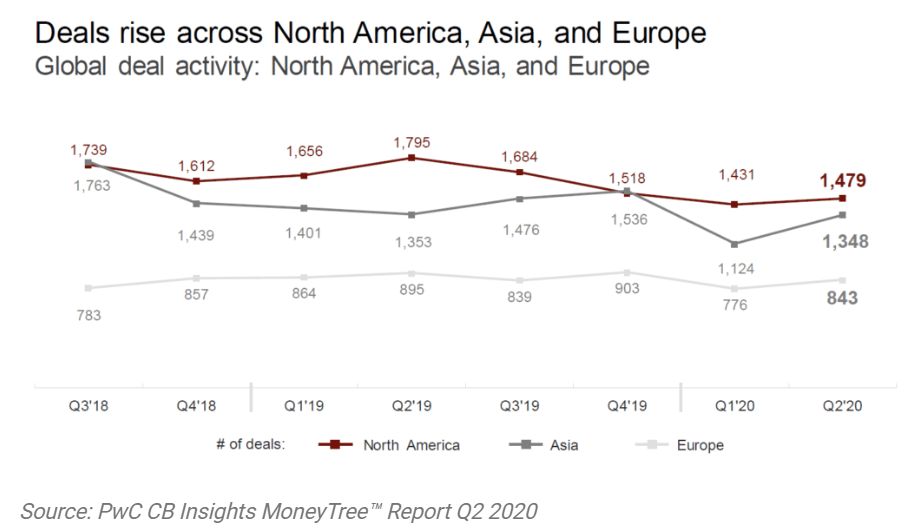

The number of deals bounced back in Q2. According to CB Insights, deal activity in Asia rises 20% in Q2’20, compared to 9% in Europe and 3% in North America.

CB Insights also comments:

“The recovery in the second half of 2009 produced several companies that introduced industry-shaping technologies and business models. For example, Uber raised $250K in seed funding in Q3’09, while Credit Karma raised a $2.5M Series A in Q4’09.”

“This year to date, startups developing supply chain and logistics technology have attracted the largest year-over-year increase in deal activity, followed by startups in digital health. Investment in these sectors is one indication that Covid-19 is accelerating the evolution of these industries, and transformational startups may emerge.”

Digital health funding shatters records with $6.3B

“Digital health received $6.3 billion in funding in the first half of 2020, shattering all previous funding records, according to a new report from research firm Mercom Capital Group. The amount is a 24% increase from the first half of 2019.”

“Telehealth, perhaps unsurprisingly, received the most money as the COVID-19 pandemic drove unprecedented virtual care adoption, with $1.7 billion in funds.”

“However, the pace of funding slowed in the second quarter with $2.8 billion across 161 deals, a 23% decrease compared to the first quarter and an 11% dip year over year.”

“The slowing momentum in March and April didn’t affect telehealth, an industry that’s seen unprecedented growth as patients turn to digital solutions for their healthcare needs to avoid potential virus transmission in hospitals and doctor’s offices. Telehealth has received more than double of the next closest sector.”

“Virtual care companies received $962 million across 50 deals in the second quarter, compared to $930 million raised in 35 deals in the first. That’s a 42% year-over-year increase, Mercom found.”

For the whole healthcare industry, venture fundraising soared to $10.4B in the first half of 2020, nearly matching 2019’s full-year record. More data and charts can be found here.

Still a high level of deal-making in the enterprise training industry

“What did mergers, acquisitions and other deals look like for the training industry this year? We still saw a high level of deal-making, perhaps reflecting the importance of training in times of crisis and the increased demand in technologies that support remote learning.”

We saw activity in technologies and services that help organizations track, manage, measure and improve employee performance.

Sales training and sales enablement service providers continued to be popular with investors. The show must go on, and so must sales — and, therefore, sales training.

Platforms that support the new world of remote work, online security and medical education are in the spotlight.

“~ $4B EdTech VC in 1H 2020 with $1.75B of that in two Chinese mega rounds. M&A back in Q2 – expect further consolidation in 2H. Many new large investors entering EdTech.”

“All hand’s on deck from EdTech and tech giants alike to support remote learning across all sectors. Tech giants across the globe are pitching in to support learners, teachers and institutions to ensure learning continues amid COVID-19 closures. Giants provide free access for educators and funding to support the continued technological transformation of education is released.”

Demand for AI-related products in education surges as learning moves to virtual. Education (K-16) has always been a slow sector to follow digital transformation, but for the first time, the pandemic has driven a seriously accelerated change.

“Funding to artificial intelligence startups has been on the rise. In 2019, AI startups received a record $28.5B in funding across over 2,300 deals. Despite the ongoing coronavirus pandemic, 2020 has seen sustained momentum — AI deals declined in Q1’20, but funding jumped by 51% from the previous quarter to hit $8.4B (Nearly 500 AI startups across 42 countries, and the mapping of AI startups in the US).” But it might recede in Q2.

For enterprises, the priority of automation will be higher than AI now, since the latter relies on good data and the justification/measurement of return on investment for some cases.

Our notes

Since semiconductors are the foundation for almost every hardware product, the monthly sales data from Taiwan’s related manufacturers is worth noting. Pay attention to the warning from Bloomberg Opinion columnist Tim Culpan: Tech’s June Jump May Lead to December Disappointment.

According to Taiwan Semiconductor Manufacturing Co., the largest contract chip manufacturer, demand for its products is being driven by 5G networks and smartphones, along with high-performance computing, such as artificial intelligence and graphics chips.

Many interesting funding events in innovative AI chips with new architectures, AI software accelerators, or quantum computing startups have been happening. There may now be hundreds of startups working on AI chips especially for gaming or special edge computing use cases.

According to some experienced investors, in the previous depression of 2008, the valuation didn’t go down until 12~18 months later. Some M&A veterans have warned that CEOs should similarly expect that the worst isn’t here yet in this depression. M&A activity has already seen sharp declines, falling to 120 exits in Q2’20 vs. 155 in Q1’20, the deal value dropped 41% according to Pitchbook.

From history, enterprises and startups had adopted more digital and automation solutions after the recoveries from previous depressions. The same may happen in this crisis. Digital transformation is accelerating, now with data and machine learning.

On the other hand, we hope to see investors to put their resources into the right companies and the right technologies to make impacts helping the society solve problems and move forward. Maybe this means they need to get out of the comfort zone. Knowledge is the power to make good judgments outside previous experiences.

Connectivity and artificial intelligence (AI) will be the biggest drivers for 2020, with an emphasis on improved reliability across all areas. New standards, new applications, and new pressures being placed on old technology will create boundless opportunities for those ready to fill the need. (Also read: Connectivity is the Key to the New Future of 2020 and Beyond)

There is a larger trend going on. “We are starting to see a need to move from the device era to an era of connectivity,” says Joseph Sawicki, executive vice president for IC EDA at Mentor, a Siemens Business. “This is evident in areas like IoT, industrial IoT, smart city, and autonomous driving. This means that verification needs to move to verification and validation of the digital twin — from the multi-chip interfaces into mechanical and real-world data — to ensure these complex systems work together.

“Digital twins, or the concept of complete replicate simulation, are the nirvana of design engineers. In 2020, we will see digital twins mature and move to the mainstream as a result of their ability to accelerate innovations. To fully realize the technology’s benefits, companies will look for advanced design and test solutions that can seamlessly validate and optimize their virtual models and real-world siblings to ensure that their behaviors are identical.”

AI is still the hottest area — “Over the last 7 years, the total venture investment in the AI/ML semiconductor sector now exceeds $2.5 billion — well over 4X the investment in the next largest market segment, high-speed communications and 5G wireless.”

People at Arm believe that “IoT will help to commercialize AI in 2020, with IoT-enabled companies using physical real-time data from IoT devices to advance their AI business goals. And as the amount of data collected from IoT devices grows and machine learning is deployed in devices and the cloud, the machine learning models will need to be updated regularly to deliver better results. We foresee the development of technology to create ‘living models’ that are constantly updated and improving AI-driven business outcomes.”

Not only IoT-based sensor data, IT-based signals, or user-generated data inputs (including form-based data and digital trail data, which can be generated by online searching, purchasing data, location data, etc.). Companies have been collecting data on people, processes, and things for several years and are now able to feed that data into ML models.

“The global AI market is entering a new phase in 2020 where the narrative is shifting from asking whether AI is viable to declaring that AI is now a requirement for most enterprises that are trying to compete on a global level,” according to the market intelligence company Tractica, AI is likely to thrive in consumer (Internet services), automotive, financial services, telecommunications, and retail industries.

Not surprisingly, the consumer sector has demonstrated its ability to capture AI, thanks to the combination of three key factors – large data sets, high-performance hardware, and state of the art algorithms. Tractica estimates that many of the top enterprise AI verticals will follow and replicate a strategy similar to consumer Internet companies. Annual global AI software revenue is forecast to grow from $10.1 billion in 2018 to $126.0 billion by 2025.

Here are the top 10 use cases in term of cumulative revenue across all industry sectors, reported by Tractica.

Top 10 AI Use Cases by Cumulative Revenues across Industries, by Tractica

Some of the most potent innovation taking place today does not involve breakthrough technologies…. but rather the creation of fundamentally new business models. In a review by Peter Diamandis, he has summed up 7 models in his new book “The Future is Faster Than You Think“. The top three are all data businesses at their core, AI is a major enabling capability.

(1) The Crowd Economy: Crowdsourcing, crowdfunding, ICOs, leveraged assets, and staff-on-demand—essentially, all the developments that leverage the billions of people already online and the billions coming online.

All have revolutionized the way we do business. Just consider leveraged assets, like Uber’s vehicles and Airbnb’s rooms, which have allowed companies to scale at speed. These crowd economy models also lean on staff-on-demand, which provides a company with the agility needed to adapt to a rapidly changing environment. And it’s everything from micro-task laborers behind Amazon’s Mechanical Turk on the low end, to Kaggle’s data scientist-on-demand services on the high end.

Example: Airbnb has become the largest “hotel chain” in the world, yet it doesn’t own a single hotel room. Instead, it leverages (that is, rents out) the assets (spare bedrooms) of the crowd, with more than 6 million rooms, flats, and houses in over 81,000 cities across the globe.

(2) The Free/Data Economy: This is the platform version of the “bait and hook” model, essentially baiting the customer with free access to a cool service and then making money off the data gathered about that customer. It also includes all the developments spurred by the big data revolution, which is allowing us to exploit micro-demographics like never before.

Example: Facebook, Google, Twitter—there’s a reason this model has transformed dorm room startups into global superpowers. Google’s search queries per day have risen from 500,000 in 1999, to 200 million in 2004, to 3 billion in 2011, to 5.6 billion today. While more users are becoming aware of the valuable data they exchange in return for Google’s “free” search service, this tried-and-true model will likely continue to succeed in the 2020s.

(3) The Smartness Economy: In the late 1800s, if you wanted a good idea for a new business, all you needed was to take an existing tool, say a drill or a washboard, and add electricity to it—thus creating a power drill or a washing machine.

In the 2020s, AI will be electricity. In other words, take any existing tool, and add a layer of smartness. So cell phones became smartphones and stereo speakers became smart speakers and cars become autonomous vehicles.

Example: We all know the big names incorporating AI into their business models—from Amazon to Salesforce. But more AI startups arise each day: 965 AI-related companies in the U.S. raised $13.5 billion in venture capital through the first 9 months of last year, according to the National Venture Capital Association. The most highly valued of them all is Nuro, a driverless grocery delivery service valued at $2.7 billion. Expect AI to continue transforming most businesses in the 2020s.

For AI as a fast-emerging technology, what business models work best is still evolving. Three business models from AI are highlighted with examples by Dan from Battery Venture here. Each has its advantages and disadvantages.

AI Business Model #1: Bolt-on – The first type of AI solution is deployed much like a product from a SaaS company, and the business models are almost interchangeable. These AI solutions sit seamlessly on top of other systems of record, like a CRM (customer relationship management) product or an ERP (enterprise resource planning) system. AI accesses data flowing through these systems, fueling business improvements over time.

AI Business Model #2: Enhanced process – In the second AI business model, deploying a new AI product doesn’t change existing workflows at all; it just turbocharges the effectiveness of current workflows by integrating AI into them. These are deep-surgery integrations and require lots of implementation work, with much-improved processes as the payoff.

AI Business Model #3: Letting the machine stand alone – In the third AI business model, the AI technology changes an entire workflow by introducing an AI-infused, better-way-to-complete-a-business-process. AI “owns” the experience end-to-end, with very little human-required assistance, giving algorithms the full control over the experience.

For enterprises, the adoption of AI can range from a fully in-house, custom-built approach to a more modular approach using pre-built solutions and tools and a fully outsourced approach solely relying on third-party vendors and teams. A significant portion of the enterprise market has neither the skill nor the budget to develop AI from scratch. There are pre-built AI solutions or tools, and consultants and contractors can customize off-the-shelf AI. Or enterprises can hire data scientists and engineers to develop, train, and run AI models.

Besides AI technical capability, the overall problem-solving modeling and strategy, coordination of execution, and the trade-off for a viable economic model will all be crucial – it means the right integration of human intelligence and AI.

From 2020 AI Talent Report published by Robin.ly, employers increasingly value non-technical attributes for AI talent. Quoted from the report: “The AI industry is facing substantial technical challenges in the face of ambiguity, and companies are increasingly seeking diverse individuals with compelling non-technical attributes, such as creativity, critical thinking, growth mindset, resilience, and communication skills.”

After all, customers or users, enterprises or individuals, don’t care about AI, they care about the value AI brings to them is worth what they pay only.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.