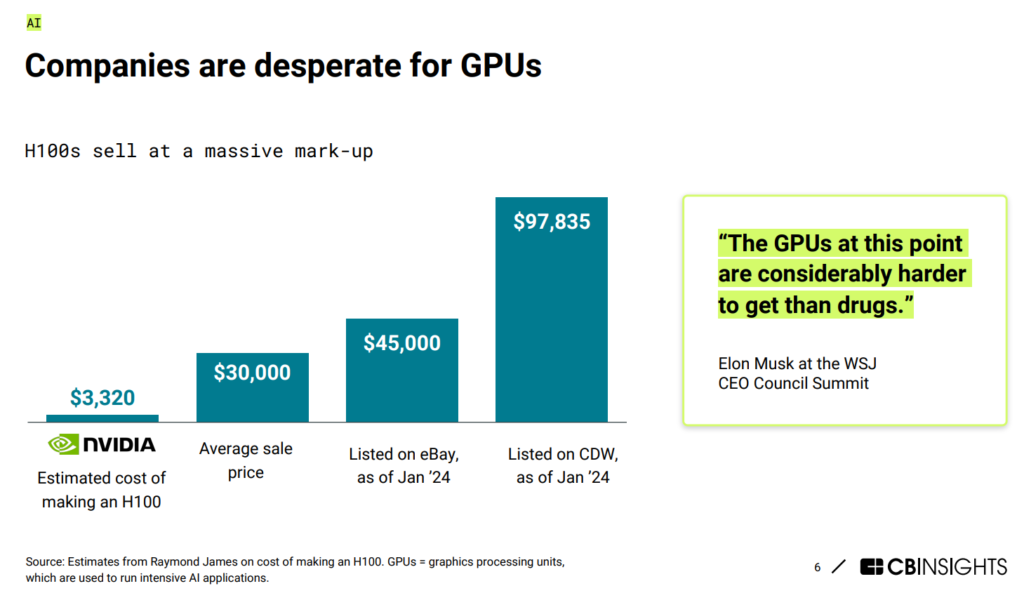

Startups link up with big tech to access their AI chips and compute power and also look outside of big tech for cheaper cloud computing. Startups building software to help AI models run efficiently on available hardware gain traction, the GPU shortage also opens the door for experimenting with novel processor approaches. Big tech is the biggest buyer, hoarding H100s in the thousands, but Nvidia’s biggest customers are also pushing their own chips. And Sam Altman, OpenAI CEO, might raise trillions of dollars for a new semiconductor fab to manufacture advanced AI chips (not to promote him here, but to show the crucial position of semiconductors in AI wars).

As reported by CBInsights, in 2023, AI startups raised $42.5B across 2,500 equity rounds., although down 10% year-over-year (YoY), it fell far less than broader venture funding (-42% in 2023). Generative AI attracted 48% of all AI funding. The US saw AI funding jump 14% YoY in 2023, fueled by mega rounds. AI deals got bigger in 2023, with the average deal size climbing 21% YoY to $23.4M, and the median deal size also held steady YoY at $4.4M (the second-highest level on record). M&A exits rebounded in 2023 to 317, a record high. The acceleration in M&A points to a wave of consolidation, as incumbents look to quickly bring AI capabilities on board. Google was the most active investor in AI in Q4’23, backing 9 AI startups. It was followed by KB Securities, Nvidia, and Plug and Play Ventures with 8 companies apiece, and then Lightspeed Venture Partners with 7.

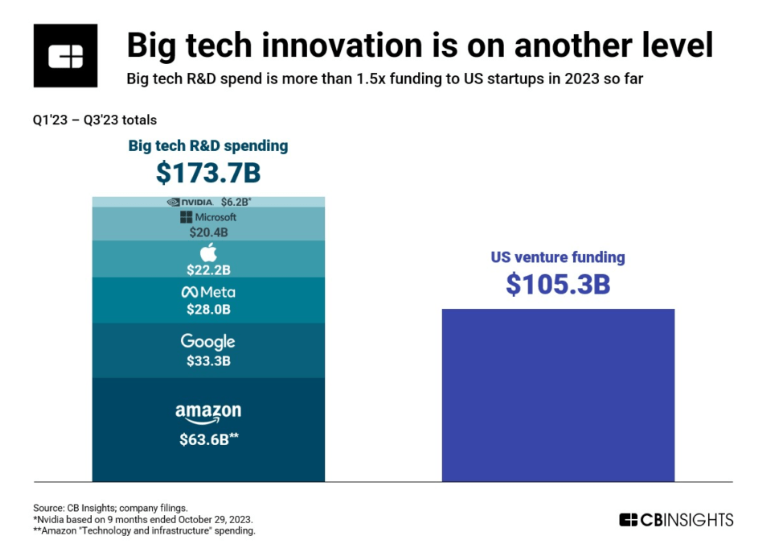

In the US, big tech companies’ R&D investment outpaces that of overall US venture funding by a wide margin. This underscores the scale these companies play in driving tech innovation. Tech giants are throwing their weight behind promising AI startups, offering computing power and funds for development, especially in the realm of generative AI. (source)

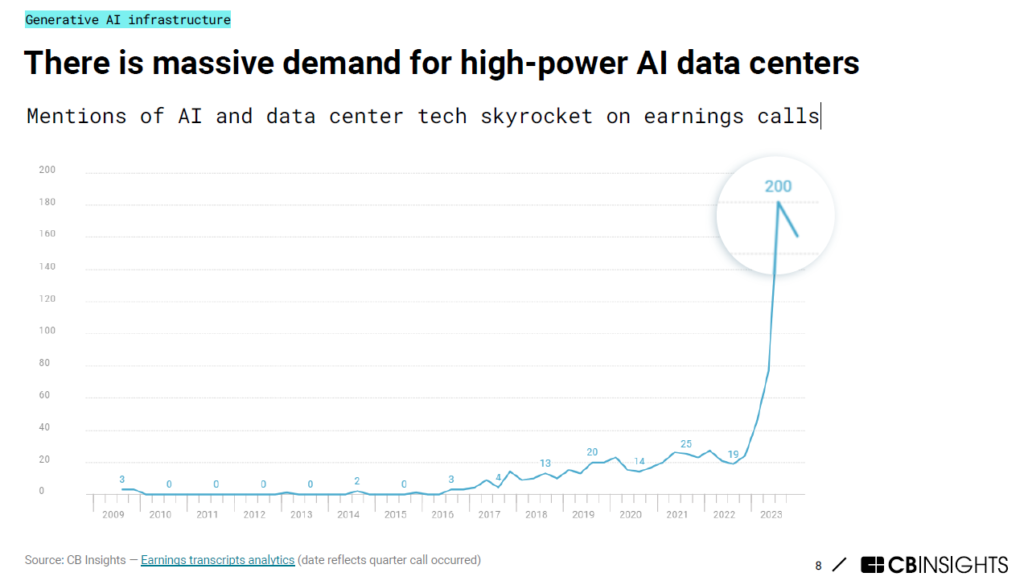

Not only big tech giants, companies are rushing to build AI data centers, and mentions of AI data centers skyrocket on earning calls.

On another advanced computing front, Quantum computing funding surged to a record high in 2023, bucking the broader venture downturn for 2 years in a row. Neutral atom quantum computers are having a breakout moment, hinting at accelerated timelines for commercialization. More enterprises are running pilots with quantum startups. Interest in the intersection between quantum computing and AI is heating up as quantum advances can enable more powerful AI models down the road.

In this AI era, access to power is a differentiator. The number one operating cost of data centers is power! Generative AI makes the data center demand from megawatt to gigawatt scale. That adds extra stress to grids or is even prohibitive without some change. And, regulations will require disclosure of carbon emissions, sustainability is more than a buzzword. There is evidence that LPs are aware of the scale of data center opportunities, and its power hunger issue (also water). Using a combination of grid-sourced power and a portfolio of other renewables, small modular nuclear reactors, wind turbines, and batteries are all possibilities. (more)

The other differentiator is semiconductor capability, this topic might take a series of posts, including advanced packaging techniques, advanced semiconductor manufacturing nodes, new circuit architectures, new materials, photonics, and more. The White House on Feb. 9, 2024, announced the U.S. government’s plan to spend $11 billion on semiconductor-related research and development and said it was launching the $5 billion National Semiconductor Technology Center. NSTC will establish an investment fund to help emerging semiconductor companies advance technologies toward commercialization. (source) Will this matter to the international semiconductor sovereignty race that started quite a while ago and now AI is added to the race?