Climate tech companies just had their best quarter for fundraising in almost two years, drawing $16.6 billion. Venture capital investment into climate tech is doubling YoY, but the funding gap is not closing fast enough.The first question about investing in climate tech comes into mind – Is this category a capital-intensive play? So, many investors choose only climate software. Actually, there are many variables in answering that question.

One of questions we’ll ask startups is – what’s your capitalization plan? It will impact life or death, speed of growth, capital efficiency for startups, and returns for investors. There are strategies for partnerships and business models to consider for a less capital-intensive growth path. And, when to exit and how? In this panel, we like to cover capitalization and financing strategies in different stages for climate tech startups.

About ClimateTech Investor Panels – This is for accredited private equity angel investors, venture capitalists, and corporate/institutional investors to share insights and investment opportunities and catalyze collaboration to help ClimateTech startups.

Speakers

Paul Burgon, Co-chair of Keiretsu Forum CleanTech Committee, GP of Exit Ventures – Paul is a dynamic operations and investment executive who has invested over $3 billion in almost 100 different companies at high rates of return. Paul balances 1) strategic analysis and strategy development, 2) creating and implementing processes that map to company strategy and 3) team leadership, consistent execution and continuous improvement to create outstanding results.

Karen Sheffield, Finance Director at Visa, Founder & Managing Partner of Pachamama Ventures – Karen is a managing partner of a venture capital firm investing in US early-stage climate tech companies. She is also a Finance Director at Visa and has previously worked for PepsiCo and American Airlines. A self-described operator turned investor, Karen began angel investing 3 years ago and, ever since then, has dedicated much of her time to uncovering opportunities in unlikely places. Karen holds a double degree in Finance and Economics from Texas Christian University (TCU) and an MBA from The University of Texas at Austin.

Interviewed by Jessie Chuang, the topics cover 3 major parts:

Funding gaps and sources for ClimateTech startups and projects

Business and partnership models deciding capital intensity & plan

When to exit and how

Takeaways:

Karen:

I grew up in Peru, and in the country, climate impacts a lot of everyday decisions we make, that’s why I am so passionate about climate investments.

Early-stage startups going to build a proof of concept (POC) need to get initial funding from friends and families, angels (several angel groups focusing on climate tech or impact investing), and government grants – there are so many now for climate tech companies, including IRA and more. Talk to grant writers to help you. Getting grants is hard, but getting funding from VCs before POC is even harder. Non-dilutive funding sources such as grants from governments are crucial for early-stage companies. and now more foundations and family offices want to invest in climate startups. Catalytic capital funds emphasize more on impact instead of maximizing financial returns solely. After you have revenue, there are revenue-based financing mechanisms that can help.

I have 15 years of experience working in Fortune 500 companies, I’ve witnessed the interest in building corporate VCs (CVC) growing significantly. Visa and Pepsi all have CVCs. Most CVCs might take a board seat if they invest to guide the startups, they have very broad interests, not limited to their current business lines, and have lots of funding to experiment. The chief sustainability offices (CSO) in large companies want to partner with climate tech innovators and achieve more than ESG compliance. Of course, there are pros and cons to consider when working with CVCs or corporate partners.

Paul:

The best outcomes in climate tech happen when companies can align their development milestones with their capital strategy.

A big difference between the cleantech 1.0 era and now is that the capital stack for climate tech has been developed rapidly and much more mature in the past 5-7 years. There are billions of hardware or cleantech funds, we see CVCs exploding, we see customer-financing models (customers as investors to build win-win outcomes, be creative, and build partnerships with customers), DOE’s loan office can support commercialization stage projects, and there are growth funds and infrastructure funds looking to back hard tech, etc. These didn’t exist 5-7 years ago, all are narrowing funding gaps substantially for first commercial operations. Especially CVCs can become your potential acquirers, so, look at companies in the ecosystem, and build partnerships.

Funding first commercial productions is still the largest funding gap risk. Although not as fast as we like, we do see that large infrastructure funds are coming down and VCs are going up to narrow the gap and reduce the capital intensity of climate tech startups. Also, a lot of innovations aren’t really as capital-heavy as most people imagine.

Paul wrote the following supplementary notes for reference.

Quote from a large climate tech grant writer: Grants are the quintessential way of filling these valleys of death with patient, risk-tolerant, non-dilutive capital. Government grants have historically done a fairly good job in earlier stages with technology risk by supporting R&D. More recently, with the massive flood of public funding into the climate space, there is sufficient funding for the government to put tens and even hundreds of millions of dollars behind a single project, enabling climate tech companies with high CapEx to undertake the large-scale demonstrations or first-of-a-kind deployments that bridge the commercialization valley of death.

Examples of investors with deep pockets for growth and physical assets are starting to raise and deploy investment vehicles earmarked for climate:

Mega-firms: Mega-shops like Brookfield, TPG, Apollo, KKR, Carlyle, Stonepeak, and Blackstone are also flocking to climate raising tens of billions to finance the net-zero transition.

DOE Title 17 Clean Tech Loan Program:

The Title 17 program can support technologies at each deployment milestone—first-of-a-kind deployments that solve applied engineering challenges; follow-on deployments that establish engineering, procurement, and construction excellence and lower total project costs; substantial scaling of deployment and manufacturing capacity to drive advancement along the learning curve; and education of commercial debt markets to enable broadly available debt financing.

Commercially ready technology has been demonstrated at near commercial-scale under expected process conditions with results supporting the expected performance of the proposed deployment. Performance data from testing at pilot and demonstration scales (confirming at least a Technical Readiness Level 6) must have been performed and be available for review in order to confirm commercial readiness. Applications will be denied if the proposed project is for research, development, or demonstration.

No minimum loan amount. It can usually cover 50-70% of eligible project costs, and loans for up to 30 years. Low interest rates. Check out the criteria here.

Thoughts on how and when to exit:

There’s no perfect answer for when to exit. Some people sell too early and leave a lot of money on the table. There are also many, many stories of startups and boards wanting to hold on and try to go public or sell for a billion dollars, and they end up losing a lot of money or almost everything a few years later due to new competitive technology, the team falling apart, or whatever.

In my opinion, you should consider a few basic things in deciding the right time to sell:

The required return of the founders and the key investors/board. Have they made enough money to justify the time and investment?

What are the technology, market and other risks that could derail the future success of the startup and create a loss scenario? You need to be very honest with yourself on this point, most startup teams are way too optimistic about their near-total invincibility in the next several years. There are always big things that can go wrong, even the unknown factors that aren’t visible today.

Do you have a realistic exit opportunity to pursue in the near to medium term? Is an exit a viable option?

Is the team ready for an exit? Sometimes people factors can preclude a successful exit. The team has to be ready, presentable, and complete.

Is the business ready? Are major customers happy, is the business litigation-free, large problem-free? Are major contracts all renewed, not about to expire? Get due diligence issues cleared up before starting the exit process.

If all of these issues are a go, then I would probably err on the side of exiting sooner rather than waiting of a perfect scenario and perfect valuation. Don’t be greedy, take a win, and stay on with the new owner for a while, maybe a long while, or go to your next big thing in my opinion.

How to exit

How to exit is a completely different podcast. I have an hour podcast on just how to exit. If you are ready to exit, you need great advisors and a board that is very experienced in the tactical best practices of exits.

About Global League

Global League is a vetted network of accredited and professional investors collaborating on We select startups from top seed investors(VCs/angel groups) and build a disciplined process to get collective intelligence for investments and venture building. Collaboration and co-investing are our core strategies to connect silos and help the most impactful ventures.

China leads the world in energy transition investments (led by the state government and corporations). In 2022, China splurged more than 500 billion U.S. dollars into technologies like solar and wind energy, batteries, and electric vehicles. This was roughly four times more than U.S. investments. In 2021, European countries invested $219B in energy transition, about double the amount of what the US invested ($114B), according to the World Economic Forum. Of course, the Whitehouse has established the Inflation Reduction Act (IRA) in 2022 as a game changer. Furthermore, US startups received VC funding in ClimateTech more than in other regions – the U.S. received the largest share of global climate tech VC funding in 2022, at 41 percent. (according to Statista)

Interviewed by Jessie Chuang, the interview questions include:

Please introduce SWAN Impact Network (the most active impact investing angel group in the US).

Which nascent sub-sectors of climate tech have the most promising potential? (what sub-sectors are too crowded?)

How do you identify and evaluate them, and how do you do due diligence?

What are the risk factors for today’s climate tech startups? How do you de-risk them? The strengths of the US market?

What is your portfolio-building strategy in climate tech investing?

Takeaways:

SWAN was started in 2016 to invest in for-profit impact startups. The strength of the network is the deep experience of the angels in the network and their passion for helping our portfolio companies succeed. We work on a quarterly basis and we receive between 50-140 applicants per quarter from all over the US. We usually end up investing in 1-2 companies per quarter.

In a recent Climate Summit hosted in Houston, the good news is the IRA will pour around $1.2T into this space in 10 years, it’s not a cap, it’s a projection!

There are a number of different sub-sectors in climate tech that we believe are very promising. The first is improved efficiency, this will most likely be in electrical applications, but could also include things like ICE engines, industrial processes, water, construction, and building maintenance. Sometimes these interim solutions that will get us to an electrified future are overlooked. We also like solutions that combine innovations in hardware and software, giving us two potential technology moats. For example, solar or wind energies combined with AI/ML or algorithms could be promising. Lastly, we are excited by startups innovating inchemistry and material science that help remove carbon and/or produce more sustainable products. There are some areas we think are too crowded, including battery chemistry and carbon tracking software.

We have a relatively standard process that we use. We see a lot of startups that we meet at events or accelerators, are already engaged with one of our many partners, or apply to us directly. First, we make sure they fit our thesis and are in a stage that makes sense for us, and are raising an amount we think makes sense. We then add them to our process which starts with an introduction with one of us on the team and a review of their documents. We evaluate their impacts, financial return potential, deal terms, product-market fit, and most importantly the team.

How do we de-risk? The first is validation by customers, for example, they have paying customers, strategic partnerships, or at least a letter of intent (LOI). And if they have obtained government grants, that’s a very positive signal, since it’s non-dilutive funding with resources and expertise. Also, we can analyze investors – what other investors have invested, especially from potential future acquirers, even only a small amount. There are macro or market risks not controllable by startups, so the team is the most crucial factor, they must be competent to handle new challenges. Furthermore, we want to see the offering is so compelling, that it’s a must-have, not nice-to-have.

We mainly invest in US startups, because the US has a global influence, and governmental risk, market risk, and supply chain risk are minimized as much as possible in the US. But we’re living in a very global world, so we ask – how global is your supply chain? Do you have backups for your critical parts? Even if it’s not realistic for early-stage startups, it’s something you should consider when making investments.

Early-stage investors, either venture capitalists or angel investors, a portfolio-building strategy is needed – consider investing in 10-20 companies in 3-4 years because a lot of risks are unknown. It’s suggested to diversify across different sectors, geographies, genders, and backgrounds of founders, and add some companies without technology risks – the technology isn’t new, but the application or go-to-market strategy is novel.

About ClimateTech Investor Panels – ClimateTech is hard for investors not only because it’s mostly deep tech, but also because the variables for unit economics and adoption readiness are evolving. We interview one ClimateTech investor every Friday, a 30-minute Zoom meeting without live-streaming, we’ll do a briefing after every interview to be shared with broader networks. Join Zoom meetings to talk to speakers, or invite others to join the conversation/follow insights (Sign up).

Half of the largest European venture capital deals in Q3 involved climate tech startups as the sector has seen less severe declines than others in VC dealmaking. A total of €9.1 billion (around $9.6 billion) was invested across 748 deals in the first 9 months of this year, according to PitchBook‘s Q3 2023 European Venture Report. This represents a fall of 42.8% for deal value and 38% for count compared to 2022. (FinTech and Software saw >70% declines)

Jørn Haanæs, Investment Director and Partner at Katapult VC (HQ in Norway) shared his view on climate tech with us on ClimateTech Investor Panels.

Katapult VC is a global investment company focusing on early-stage impact-driven technology startups. Over the last 5 years, Katapult has made 169 investments in impact tech startups from 47 different countries. Katapult invests within three investment verticals: Ocean-, Climate- and Food-tech. Katapult has run nine flagship accelerator programs and three corporate accelerator programs. Jorn has been with Katapult for about 3 years managing the climate fund, has reviewed 1000+ and interviewed hundreds of startups every year; before this, he was a successful entrepreneur who exited from his B2B software startup. He believes the climate challenge is the most pressing challenge for humans, and also will be the most profitable opportunity.

Interviewed by Jessie Chuang, the interview questions include:

Major public investments (procurement) and policies driving ClimateTech private investment momentum in Europe, and the timeline of impact.

Which nascent sub-sectors of climate tech have the most promising potential? (What sub-sectors are too crowded?)

How do you identify and evaluate them during diligence? (Invest after PMF, revenue?)

Please introduce Katapult and talk about your previous and recent investments and portfolio-building strategy.

What companies in your portfolio are growing faster than others? Lessons learned? Does impact investing sacrifice return for impact?

Takeaways:

In the climate tech space, we usually look at energy, mobility, cities, and enabling technologies. Cities and urbanization (urban tech stack) are the driving forces for reducing CO2 footprints. It relies on companies and consumers to adopt new innovations better than the previous ones, so you must make better or cheaper products. Climate tech needs to make its unit economics work.

Now the regulatory framework driving this is strong, but we mostly invest in B2B, less in B2G. CO2/externality taxing has started to influence the market to recognize climate tech startups, and we need to respond.

For seed-stage investors, we need to look at a very large number of startups and invest in a portfolio of enough deals in different opportunities. The power law is true in the early and later stages. Finding winners is much more important than negotiating the price. Identify winners and invest early, make them ready for series A investors, and we’ll generate returns.

The acceleration model after investing has been proven to be very effective and valuable, startups can fix their most important problems during the program (note: it can be remote). Katapult’s portfolio companies have a very high survival rate of startups – only 23/169 failed.

Overall Katapult has an average net IRR across funds of around 41%, which proves that the financial return of impact investing doesn’t need to be compromised. Actually, returns come from impact! Impact investors are different from philanthropy investors, and should not sacrifice returns for impact.

Katapult started as an impact investor in 2017 backing startups working on both social and climate issues, no one was doing that back then. These companies need much more than capital, and Katapult’s main value is connecting them with knowledge, networks, and opportunities, also helping them understand, classify, and communicate their impacts to drive value creation. Both Africa, Ocean, and climate funds are built from insights identifying under-invested areas, and applying the same method to invest and grow.

We invest in mostly revenue-generating companies, revenue-generating isn’t product-market-fit (PMF), and most seed companies don’t have PMF. We try to help startups understand how to run structured experiments to get to PMF. There are two very important distinguishing factors that de-risk startups: the first is closing the first customer to have revenue, and the 2nd is making sure you have quality revenue, don’t scale too fast, and continue to do experiments.

The boom and bust in previous clean tech cycles are faults of our financial system. We are going to decarbonize the entire economy, the opportunity is huge! The first order is energy since it goes into everything else.

About ClimateTech Investor Panels – ClimateTech is hard for investors not only because it’s mostly deep tech, but also because the variables for unit economics and adoption readiness are evolving. We interview one ClimateTech investor every Friday, a 30-minute Zoom meeting without live-streaming, we’ll do a briefing after every interview to be shared with broader networks. Join Zoom meetings to talk to speakers, or invite others to join the conversation/follow insights (Sign up).

The London School of Economics reports more than 5,000 national climate laws have been passed worldwide over the past dozen years. Leading the way: The U.S. Inflation Reduction Act (IRA), which directs nearly $400 billion to energy innovation. Carrots, sticks, and corporate voluntary actions to reduce their emissions, this ClimateTech wave is global and unprecedented, different from the previous “CleanTech 1.0” more than a decade ago. US people often think Europe is more advanced in climate actions and investments, but the U.S. IRA has claimed a leading position as a change maker now. Has it? Let’s take a deeper dive into the climate of ClimateTech’s public and private investments in both.

Speakers

Oct., 27th

Jørn Haanæs, Investment Director and Partner at Katapult – He is passionate about tech and culture, and how it affects everything around us. His background is in the tech and entertainment industries, in building entrepreneurial ecosystems (Startup Director of Oslo Business Region) and serving as a CEO for a VC-backed startup with exit (Soundrop). Katapult invests in global seed-stage climate tech. His mission is to facilitate entrepreneurs and help startups grow through impact investing.

Nov., 3rd

Juan Thurman, Director of SWAN Impact Network – Juan is an early-stage investor, board member of numerous startups, and the director of SWAN Impact Network, he is dedicated to helping early-stage clean tech and climate companies get to the next level. He’s a GP for a new ClimateTech fund.

Host: Jessie Chuang – Jessie is a startup advisor with US and international teams, an angel investor, and the managing partner leading Global League. Her previous experience includes 10+ years in semiconductor R&D and team management, and another 10+ years in corporate consulting on digital transformation and talent development technologies.

About Katapult VC

Katapult VC is a global investment company focusing on early-stage impact-driven technology startups. Over the last 5 years, Katapult has made 178 investments in impact tech startups from 47 different countries. Katapult invests within three investment verticals: Ocean-, Climate- and Food-tech. Katapult has run nine flagship accelerator programs and three corporate accelerator programs. In 2021, Katapult launched the Katapult Foundation with the aim of building a larger network around impact investing. Katapult also hosts the annual Katapult Future Fest in Oslo, bringing together founders, investors, and some of the most prominent figures within impact investment

About SWAN Impact Network

SWAN is a is a 501(c)(3) non-profit. The angels at the SWAN Impact Network are bound together by a passion for making the world a better place by supporting dynamic startups that are striving to address serious challenges that our society faces. SWAN focuses on companies who expect to deliver measurable social or environmental impact, and who also have solid plans for financial success. The SWAN Impact Philanthropic Fund allows both accredited and non-accredited investors to make charitable donations which are then used to invest in impact startup companies.

About Global League

Global League is a global investor fellowship to build a network of intelligence plus a decision-making process proven by top investor networks or VCs with an average IRR > 25%. We select startups from top seed investors(VCs/angel groups) and build a disciplined process to get collective intelligence for investments and venture building. Collaboration and co-investing are our core strategies to connect silos and amplify global impact on the health of humans and our planet.

About Wise Ocean

Wise Ocean builds up a global network to connect proven startups or scaleups, industry leaders, corporate innovators, ecosystem partners, and investors for impact and profit-making. For international startups entering the US market, we will help navigate US resources (partners or accelerators) matched to your needs, for US companies looking for Asia manufacturing or market partners, we connect with Taiwan partners.

About Enventure

Enventure is a holding company with subsidiaries of PE, VC, consulting, and non-profit entities that serve different investment methods, sectors, and audiences to empower businesses with capital, unparalleled strategic insights, and a specialized network. Our approach is uniquely hands-on, providing end-to-end investment & consulting services.

Note: Interview questions will be collected and shared with speakers before panels, briefings and recordings of panels will be shared with broader networks afterward. Sign up to get meeting invites or briefings/recordings.

The IRA allocated around $400 billion in federal dollars for clean energy projects. It aims to incentivize the manufacturing or projects of clean energy in the US through multiple tax credits, targeted mostly toward solar and wind operations.

The Advanced Manufacturing Production Credit (AMPC) affords manufacturers tax credits for producing qualifying devices needed for clean energy projects. The amount of the credit is determined by the device, its specific function and its capacity.

The Production Tax Credit (PTC) grants tax credits to wind projects up to 2.6 cents/kWh of energy that they produce.

The Investment Tax Credit (ITC) incentivizes solar energy companies to further invest in their U.S.-based operations by offering up to a 30% tax credit on “energy property,” a definition that has been newly broadened with this act.

The PTC and ITC tax credits do come with some fine print, such as a three-year window in which companies must begin construction to qualify. There are also prevailing wage and apprenticeship requirements that determine whether companies qualify for all the aforementioned rates or just 20%. These tax credits serve as massive incentives for companies to expand their operations in the U.S. The IRA also encourages households and individuals to invest in clean energy products through tax breaks.

A little more than one year after the passage of the IRA, what has happened to the clean tech landscape? Manufacturing dominates the major theme. (reference)

There’s a battery boom across the country—the IRA tax credits available are projected to cut the total cost of U.S.-manufactured battery cells and packs by one-third. 91 companies have announced new battery projects totaling $77.7 billion in investments.

Eight of 25 new projects in clean tech are in semiconductor manufacturing. The others range from sustainable aviation fuel to manufacturing tools for home energy efficiency. All together totaling in 133.38 billion invested.

About 65 new electric vehicle projects totaling 44.1 billion in Domestic EV production investments were announced.

Private investments might surpass the public funding, in one year more than 270 new clean energy projects with private investment totaling $132 billion were announced according to an August report from Bank of America Global Research. More than half of them went to EVs and batteries, the rest went to renewable energy, grid storage, carbon capture, utilization and storage and clean fuels. BoA expects these investments to create more than 86,000 jobs, including 50,000 in EVs.

Capital from the IRA will mostly flow toward established companies, but private investment, like venture capital, is finding its way to startups across all stages. Many startups have cropped up to offer auxiliary services to larger industries. The number of startups has risen significantly, including solar, stationary, and long-duration energy storage, energy transmission, hydrogen energy, carbon capture and sequestration, domestic EV manufacturing, and EV charging.

American companies restored almost 350,000 manufacturing jobs in 2022 — a 25 percent increase from 2021. If looking back on a one-year timeline from August 2022 to August 2023, the manufacturing sector job growth number is around 123,000. (reference)

Besides IRA, the CHIPS Act supports a domestic semiconductor supply chain for the U.S. Clean energy manufacturing, such as solar panels, wind turbines, and electric vehicles (EVs), is heavily dependent on semiconductor chips at the core. Even this $1B plant – New-Zero 1 – aimed to turn corn into jet fuel using wind and solar energy needs semiconductor devices. Now US semiconductor is booming synergetically to spring the unprecedented clean energy sector expansion.

Transistors, such as IGBTs and SiC MOSFETs, play a critical role in perhaps the most important device within all these machines: the inverter. Wind and solar inverters convert DC energy into AC energy (AC) to allow the electricity to be distributed through the grid into homes and facilities. In EVs, the inverter plays the same role, turning the DC energy from the car battery into AC energy used to power the car’s various electronic components. Those wind and solar inverters are qualifying AMPC devices to receive tax credits to reduce the overall manufacturing cost. Along with transistors, another type of semiconductor that could see higher demand is multilayer ceramic capacitors (MLCC). A significant portion of MLCC demand is driven by the automotive industry, specifically as it pertains to EVs. A single EV can contain up to 18,000 MLCCs, and as EVs become more sophisticated, that number is expected to grow rapidly.

These are just a few examples. In general, semiconductor manufacturing is a national security priority now, especially owning/onshoring advanced semiconductor manufacturing capability. One Year after the CHIPS and Science Act, the White House marks historic progress – Companies have announced $166B in investments in semiconductors and electronics on top of $52.7B promised by the Act. The report also summarizes actions supporting regional economic development, investing in innovation, building jobs, and workforce pipeline in semiconductor manufacturing. As AL/ML is integrated into more verticals, the race for computing speed, power, and efficiency as well as emission reduction is driving the advanced semiconductor frontier innovations in the US. Microchips that can handle AI workloads are in high demand for data centers, autonomous vehicles, inferencing at the edge, and more. Semiconductor is an enabler and technology multiplier to all. It drives a whole supply chain economics and its high barrier drives advancements in many technologies. Open innovation strategy is common in this industry.

Manufacturing presents a huge opportunity for applied machine learning. It’s a massive space — north of $5 trillion in the US alone — and increasingly data-rich. Manufacturing investments might be too capital-heavy that small VCs and angel investors can’t participate in, but the ecosystem is huge. Capital-light value providers from design support, metrology, new materials, sustainability, digitalization, optimization, and automation for manufacturing factories, and even workforce development could be opportunities for small private investors. However, the knowledge barrier is very high.

Join Global League to learn about potential investment opportunities in these.

Achieving deep emissions reductions in heavy industry (cement, steel, and chemicals production) can be challenging for several reasons. Carbon capture, utilization, and storage (CCUS) technologies might be among the cheapest abatement options – or the only option. For example, in the case of cement production, where two-thirds of emissions are from chemical reactions related to heating limestone, CCUS is currently the only scalable solution for reducing emissions. And in the iron and steel sector, production routes based on CCUS are currently the most advanced and least-cost low-carbon options, the same in the production of some important chemicals such as ammonia, which is widely used in fertilizers. More policies are supporting the carbon capture adoption now. (read more in IEA writing)

The cost of CCUS might be reduced as the maturity and infrastructures are improved, but that needs heavier investments and longer time horizons, and maybe not be suitable for most VCs or angel investors. Capturing CO2 is cheaper if compared with converting it from its capture solvent into a purified tank which could be up to 10x more energetically and financially costly. CO2 storage or transportation will increase operating costs or logistics burdens, the cost varies widely (data reference here). It’s better if we can utilize the CO2 immediately to create some valuable products which can be sold to create income to offset the cost or even make profits. It’s part of the so-called Carbon-to-Value (C2V) – a fast-emerging and evolving category. It could be the most VC-backable sector within the broader circular carbon economy.

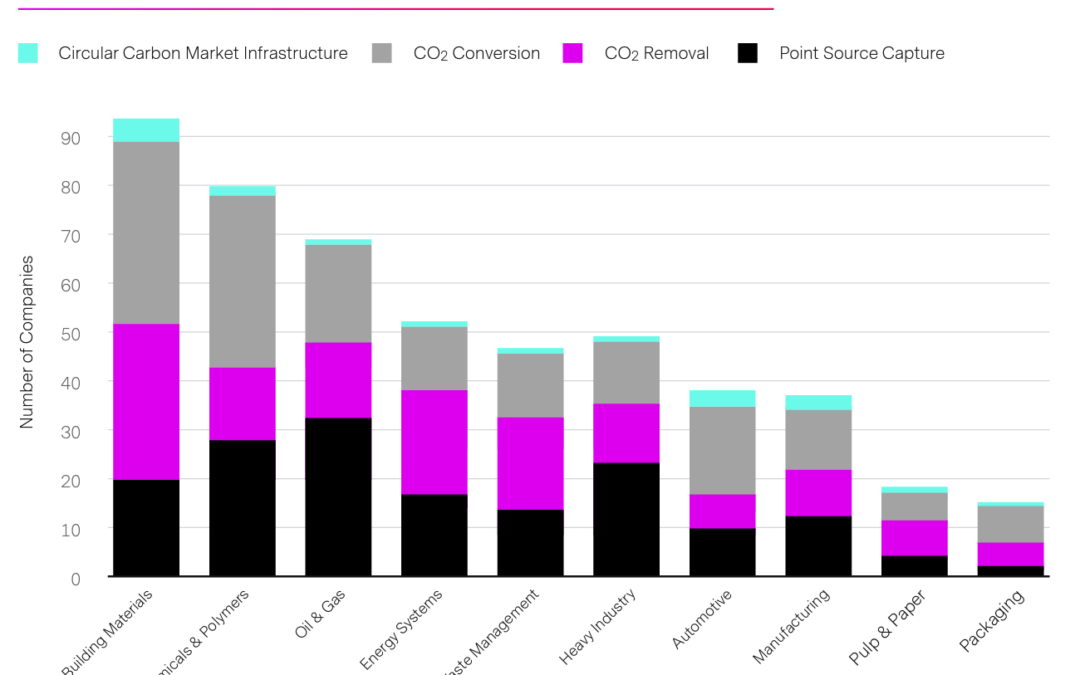

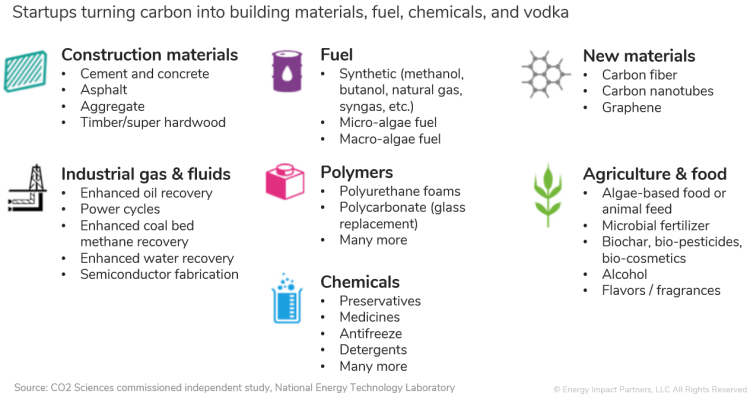

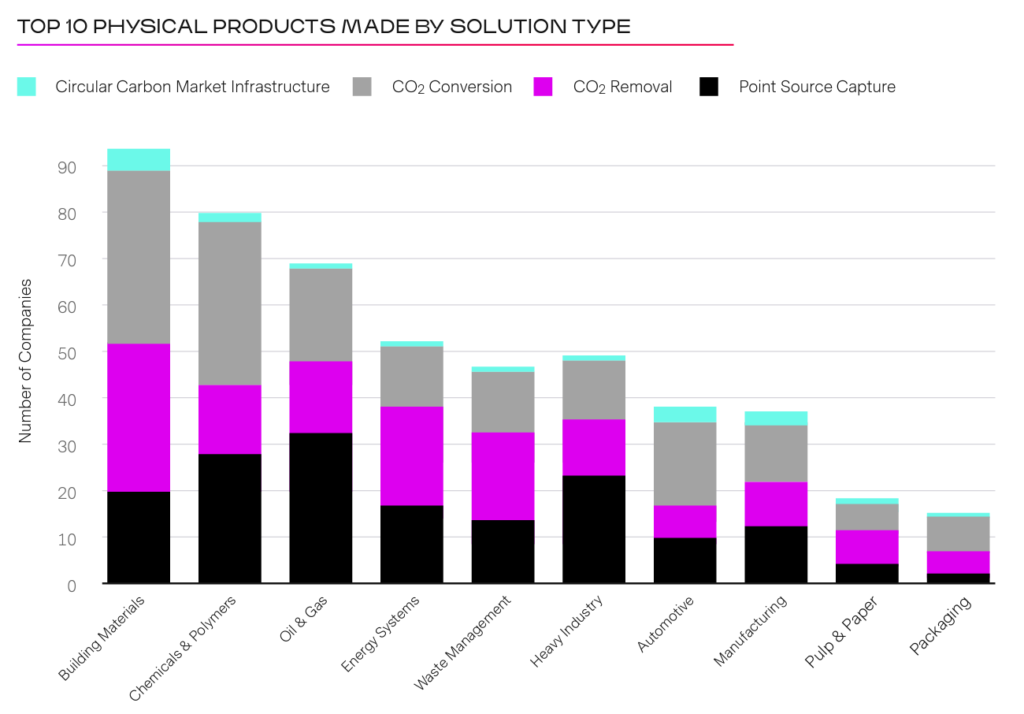

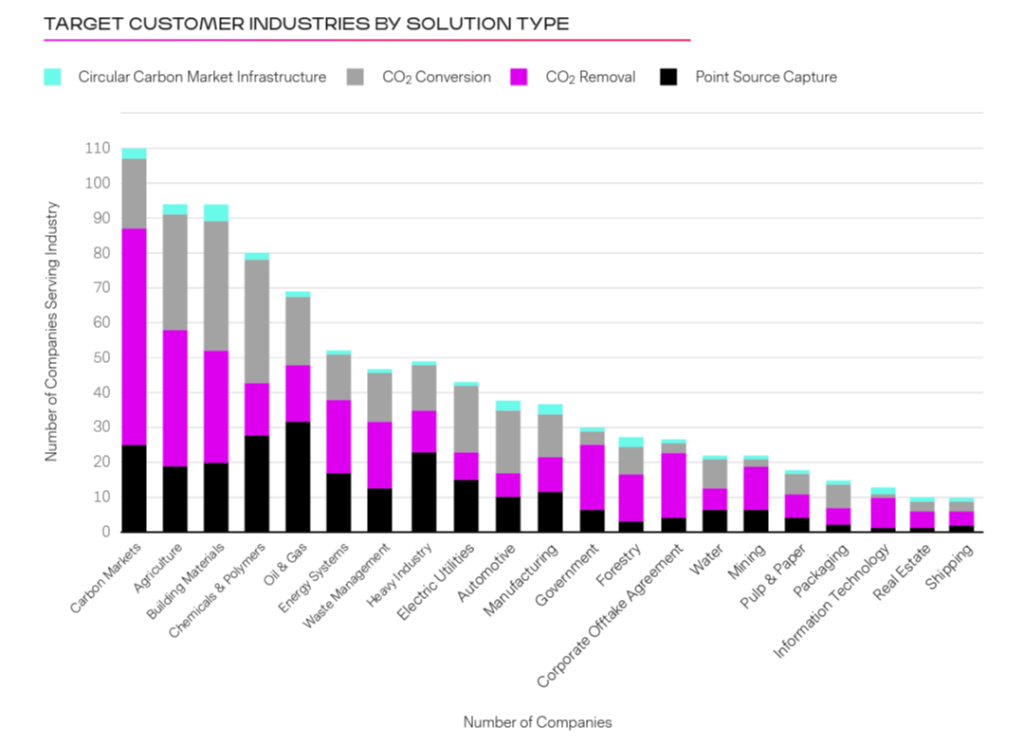

A significant amount of startups focus on carbon utilization applications, representing a very broad range of possible end products, from foods, and specialty chemicals to fuels and building materials, pictured below. There are 274 companies working on carbon conversion with some combined with other carbon solutions (removal, capture, etc) collected in Circular Carbon Network (an XPRIZE initiative) Circular Carbon Market Report of 2022.

Circular Carbon Network has been tracking new companies in the carbon space, over half of all carbon tech companies (52%) within their carbon economy index report make a physical product, either in combination with offset sales and tax incentives or as the single revenue driver. Hard-to-decarbonize sectors such as building materials, industrial chemicals, and liquid fuels will likely have the largest addressable markets (estimated at $5.6 trillion collectively). Ideal C2V solutions can plug into those industries currently lacking a pathway to decarbonization to turn carbon and other by-products into useful and valuable products. Besides, the industrial gasses, consumer goods, and biochar categories also have more than doubled in size since 2021, suggesting larger investments or demand growth for these categories.

Credit: Circular Carbon Network

Major challenges are unit economics and “cross-the-chasm” adoption. Despite a few initial adopters, corporates will be reluctant to purchase carbon-negative products purely for climate reasons. C2V products still need to be comparable or cheaper than existing materials and even then, many legacy industrial, building, or transportation companies are extremely conservative and unwilling to adopt new technologies given the scale and risk of their businesses, and some industries are regulated. Digging into different contexts including driving policies in different industries and getting opinions from industry advisors are needed in making investment decisions.

For example, the EU has passed a regulation to recognize e-fuel made from captured carbon and green hydrogen from renewable energy as carbon neutral. Without a doubt, e-fuel has a significant opportunity in the aviation industry for Sustainable Aviation Fuel (SAF) since there is not much choice. And, the Inflation Reduction Act (IRA) has transformed the SAF landscape, with the inclusion or expansion of at least three significant tax credits. As a result, many “low carbon intensity” manufacturing pathways can become cost-competitive with conventional jet fuel. Subsidies and tax credits are important, IRA tax credits are transferrable and stackable, which creates significant funding for clean energy producers. (dig deeper here)

Figuring out the financing path early is essential. Among several types of funding sources supporting these carbon tech innovations — government and philanthropic grants, project equities and debts, and private investors, funding for equities raised from private investors (PE/VC) and angel investors is the largest category. Many climate tech investors have been getting more active this year even in the overall market downturn. But there’s a huge gap between early-stage venture capital checks and the $200m+ DOE loan program scale checks, CTVC’s post on the bridge to bankability addressed potential options.

Strategic business models are very important in terms of capital efficiency. It will be very hard for startups to sell equipment or services to a slow-moving, thin-margin incumbent, especially if they need to pay upfront dollars. Building a new full-stack company doesn’t always make sense, particularly when the cost of capital is high. In the so-called clean tech 1.0 era (2006 ~ 2011), some 90% of series A investments failed to return that initial investment, per a 2016 MIT study. Of those that did succeed, market returns were found to be lower than comparable investments in healthcare or software. We as investors can learn lessons from clean tech 1.0.

Corporates need climate tech to meet their climate commitments. To accelerate decarbonization in hard-to-abate sectors, the World Economic Forum, the Office of the US Special Presidential Envoy for Climate, and Boston Consulting Group created the First Movers Coalition with 83 blue chip members that have committed to buy more than $12 billion worth of net-zero products. On the other hand, large tech companies such as Microsoft, Shopify, Stripe, and Amazon have all made decarbonization investments – either through a dedicated climate fund and/or incorporating carbon removal options to customers. Climate Action 100+, the largest investor initiative on climate change, has signed 700 institutional investors managing a combined $68 trillion in assets to commit to leveraging their power and influence to ensure the world’s largest emitters take necessary action on climate change. United Airlines even formed an investor alliance and Sustainable Flight Fund to support startups developing SAF. More than 4,000 businesses around the world are already working with the Science Based Targets initiative (SBTi) for goal setting of climate commitments. Of course, global governments set up regulations are the sticks – corporations are under pressure.

Carbon markets can help with carbon monetization to motivate the adoption. Circular Carbon Network surveyed companies about their target customer industry to further understand the potential customer bases of solution providers. In 2022 companies targeting Carbon Markets as a revenue stream made a huge jump to the top of the list as target customers for Circular Carbon startups, increasing 160% in responses. We’ll talk about the carbon market and software in the next post.

Credit: Circular Carbon Network

Join usfor more discoveries and discussions on investment opportunities and risks in the emerging carbon economy.

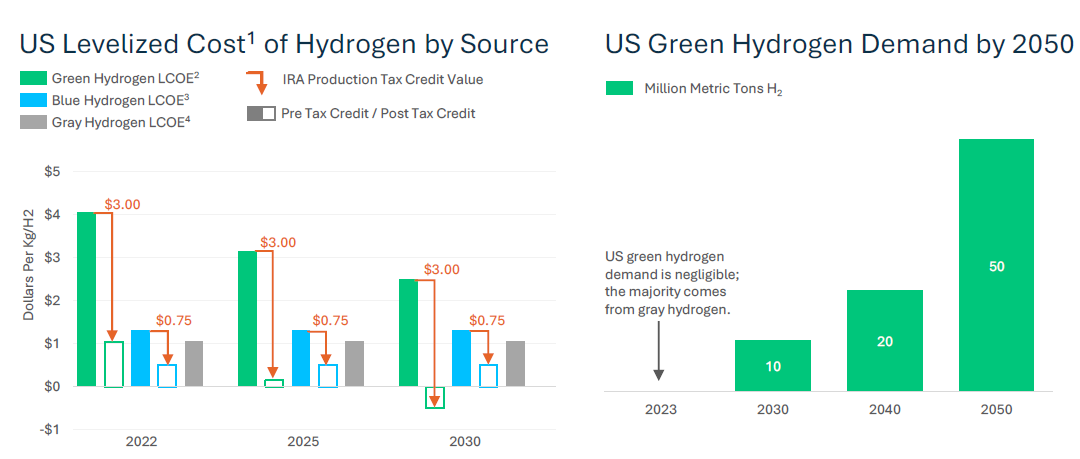

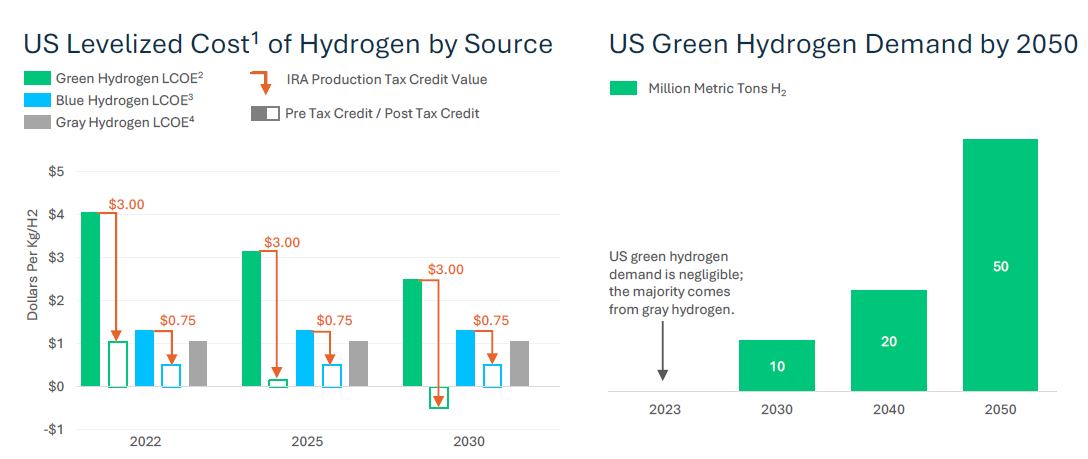

The climate crisis, the global clean energy transition, and the ‘electrify everything’ global movement are driving a massive transformation of industries and infrastructure globally. Green hydrogen has the potential to create a $1 trillion business and assist reduce more than 20% of the world’s CO2 emissions. The move to green hydrogen is being pushed by governments all over the world through new rules and incentive schemes.

Green hydrogen has been seen as the top decarbonization option for steelmaking, chemical manufacturing, and in fuel cells in medium to heavy-duty land transport. In aviation and shipping, besides replacing fossil-based vehicles with hydrogen vehicles, the EU also pushes for using e-fuel made from green hydrogen and carbon captured.

However, its high costs and the need for more infrastructure are the major hurdles. The IRA makes bold bets to unlock green hydrogen demand with production tax credits of up to $3 per kilogram. These incentives set the US up to be the cheapest source of green hydrogen in the world. For companies to qualify for the maximum tax credit, the law requires hydrogen to be produced with processes where the GHG emissions rate is less than 0.45 kg of CO2e per kg of hydrogen. For comparison, grey hydrogen produces about 24x more CO2e. Furthermore, the DOE has allocated $8B to develop six to ten regional hydrogen hubs across the US.

— From The Future of Climate Tech, June 2023, by Silicon Valley Bank

Besides subsidies, many companies are working to develop technology that can reduce the cost of clean hydrogen. especially electrolysis technologies. The two main commercial hydrogen electrolyzers currently dominating the market—Liquid Alkaline & PEM—either have low efficiency or are extremely expensive. One technology of particular interest is AEM (anion exchange membrane) electrolysis technology. AEM technology is an innovation focus area because of heap CapEx and lower OpEx with higher efficiency, and its potential to integrate directly with intermittent renewable electricity while using low-cost abundant materials.

Electrolyzer companies that have reached commercialization and are manufacturing 100s of MWs of electrolyzers are typically worth over $1B (Plug Power, Nel, Nucera). Pre-commercial electrolyzer companies with a certified, 1MW+ system design have received valuations of $200M+ (Ohmium, Electric Hydrogen, Enapter, H-Tec). Of course, there are a lot more upstart challengers working on similar technologies. No need to chase startups with hyped valuations.

We are seeing more emerging startups addressing challenges in the green hydrogen economy or building new innovations. Some examples:

New membrane-free hydrogen production technology reduces CapEx by half compared to traditional electrolyzers with higher energy efficiency.

Hydrogen purification is needed for all kinds of hydrogen generation methods, better performance and the same or lower cost is pursued.

Hydrogen dispensing/fueling infrastructure is the biggest gap to support vehicles with hydrogen fuel cells. Companies offer on-site or off-site hydrogen generation, compression, and dispensing appliance uses water and electricity to produce high-purity fuel cell-grade hydrogen, powered by renewable power. There are different solutions serving the trucking industry or consumers.

The efficient storage of hydrogen onboard trucks, ships, and planes remains one of the key challenges. Startups take the challenges of the existing hydrogen storage solutions to improve volumetric density, weight, safety, and cost. Also, a startup enables hydrogen to be stored within an organic liquid which can be handled and transported no differently than gasoline.

Producing green hydrogen and biochar from agricultural waste streams, and monetizing the carbon credits the activity generates. More than 30% of U.S. total methane and 70% of nitrous oxide emissions come from the decomposition of agricultural wastes (from DOE), this process solves it at the same time while producing green hydrogen.

Producing carbon neutral high purity hydrogen from recycled feedstocks such as plastics and tires.

Using microbes to make hydrogen from oil, the team backed by Occidental Petroleum claimed they can produce hydrogen at $1 per kilogram by injecting oil-eating microorganisms inside depleted crude reservoirs.

A hydrogen marketplace makes it easy to trade and procure hydrogen.

A capital-light approach to hydrogen logistics by transporting green hydrogen in modular capsules over the existing freight network from green production sites to airports around the world, plus conversion kits to retrofit the existing fleet with a hydrogen fuel cell powertrain.

Repurposing old fossil fuel reservoirs as sources of clean hydrogen, harnessing biological processes to convert leftover hydrocarbons from subsurface wells into usable hydrogen while capturing and storing CO2(use other microbes to lock it underground). This is called Gold Hydrogen.

Join us for more discoveries and discussions on investment opportunities and risks in the green hydrogen economy.

With most startups struggling to get funding in a cooled market, carbon capture, utilization, and storage (CCUS) companies are in a completely different pool in 2023. According to Crunchbase, over half a billion dollars has gone to dozens of upstarts this past year. Crunchbase put together a list of companies with business models tied to carbon removal, capture, and storage that last secured funding in the past year. Noteworthy themes are:

Marketplaces for carbon credits and measuring tools for enterprises, examples: Patch Technologies, Carbon Direct, Supercritical

Decarbonization of industrial materials especially cement, or carbon-negative building materials, examples: Svante, Plantd, CarbonCure

CCUS startup valuations have skyrocketed since the passing of the IRA. Silicon Valley Bank issued a nice report titled “The Future of Climate Tech” this June and placed CCUS at the peak of the hype cycle of climate tech.

This article likes to take a look at CCUS with a grain of salt. Numerous U.S. oil and gas producers have announced major CCUS projects in recent years. This includes the proposed $100 billion CCUS project in Houston under development by a group of companies led by ExxonMobil. This month (July, 2023) ExxonMobil just agreed to buy Denbury Inc for $4.9 billion (a small deal compared to its profit of $56B last year) to accelerate its energy transition business with an established carbon dioxide (CO2) sequestration operation, ExxonMobil has sought to build a carbon hub at Gulf Coast according to news, it can provide carbon reduction services quickly after this acquisition. The company already plans to store 2M tonnes of CO2 per year beginning in 2025 for Linde’s blue hydrogen and nitrogen facility in Beaumont, Texas, and has purchased a geologic permanent storage site in Louisiana.

Carbon sequestration has been embraced by oil companies including Chevron, Occidental Petroleum, and Talos Energy, which aim to capture and store CO2 underground. CCS is basically the only path for an O&G company to decarbonize while continuing its fossil fuels business. Drilling wells to store captured CO2 and managing the infrastructure to transport it allows Exxon to participate in the energy transition while leveraging existing expertise and assets.

This May (2023), the U.S. Environmental Protection Agency, or EPA, proposed a new rule to nearly eliminate climate pollution from the nation’s coal- and natural gas-fired power plants by 2040. In contrast to previously proposed regulations that required “generation-shifting” — forcing utility companies to replace their fossil fuel-fired power generators with renewables, a strategy that the Supreme Court shut down last summer — the new proposal focuses on what’s achievable using technologies like carbon capture and storage, or CCS.

Wide-scale adoption of carbon sequestration remains uncertain because of the costs and technical challenges. The advertising/comms of O&G companies don’t really match their real impact, there is still a long way to go. CCS doesn’t have a strong track record of actually sequestering carbon — especially for the power sector, where 90 percent of the proposed carbon capture capacity has failed or never gotten off the ground (source). As reported by Time, some three dozen utility companies submitted a comment to the EPA last summer highlighting the “low likelihood” that CCS would be appropriate for use in the agency’s power plant regulations. They criticized the EPA for pointing to pilot projects as evidence of CCS’s viability. “A proposed or developing project … is not proof of a technology being available,” the utilities wrote.

A large volume of captured carbon is used for “enhanced oil recovery (EOR)” – a process where CO2 is pumped into oil fields in order to push more fossil fuels out of the ground. When burned, these fossil fuels release carbon back into the atmosphere, exacerbating global warming. This is just perpetuating the use and reliance on fossil fuels. For the carbon dioxide captured injected into dedicated underground storage reservoirs, it’s questionable whether it will stay put long-term. Ramping up carbon storage would develop a vast, expensive, and potentially dangerous network of CO2 pipelines. Also, CCS fails to address other pollutants like nitrogen oxides, which could continue to come out of power plants and harm nearby communities. A major blue hydrogen project in Louisiana is currently on hold due to local opposition over a plan to store any CO2 generated beneath a lake, as some residents fear it could pollute local water resources. McKinsey advocates that strategically building carbon capture, utilization, and storage hubs near clusters of large emitters can lower costs and accelerate scale-up.

Because of the huge push to decarbonize the industrial sector, which accounts for close to one-third of total U.S. emissions and is the most difficult to decarbonize. In March 2023, the IRA launched a $6 billion Industrial Demonstrations Program that funds up to 50% of the cost of each CCUS project. This represents a $12 billion opportunity for early-stage commercial-scale projects. The main problem with direct air capture is too energy-intensive, and therefore too expensive. That will still likely be the case in five, seven, or even 10 years, in a report by DCVC they were surprised to see hundreds of millions of dollars in capital flowing into early-stage direct air capture companies, such as Switzerland’s Climeworks, Canada’s Carbon Engineering, and U.S.-based Global Thermostat.

On the other hand, point source carbon capture is emerging and evolving faster, Carbon Clean builds modular chambers that use a liquid solvent to absorb flue gas at cement and steel plants and oil refineries; Remora, which can capture at least 80 percent of the CO₂ coming out the tailpipes of semitrucks; and Osmoses, which is developing novel gas-separation membranes that could lower the cost of carbon capture. Such technologies could become affordable in the foreseeable future. How to utilize the captured carbon safely with a viable cost structure is a topic worth another deep dive. (Promising Climate Tech – Carbon to Value)

Harvard Business Review had done a survey and interviews with the vast majority of leading VC firms. Specifically, the team asked about how VCs source deals, select and structure investments, manage portfolio companies post-investment, organize themselves, and manage their relationships with limited partners. There were responses from almost 900 venture capitalists — making the study the most comprehensive to date.

They found that…

Even for entrepreneurs who do gain access to a VC, the odds of securing funding are quite low. Our survey found that for each deal a VC firm eventually closes, the firm considers, on average, 101 opportunities. 28 of those opportunities will lead to a meeting with management; 10 will be reviewed at a partner meeting; 4.8 will proceed to due diligence; 1.7 will move on to the negotiation of a term sheet with the startup; and only one will actually be funded. A typical deal takes 83 days to close, and firms reported spending an average of 118 hours on due diligence during that period, making calls to an average of 10 references.

Though VCs reject far more deals than they accept, they can be very aggressive when they spot a company they like. Vinod Khosla, a cofounder of Sun Microsystems and the founder of Khosla Ventures, told us that the power dynamic can quickly flip when VCs become excited about a start-up, particularly if it has offers from other firms.

As the investment climate has turned investor-friendly this year (2023), this panel will interview VCs about how their investment funnels and decision-making process are structured, with a focus on deep tech startups.

Topics:

Introductions of Lam Capital/Research, SOSV, TINVA, Ceres Capital and their missions and stages of startup engagement/investment

The process of deal sourcing, evaluation, due diligence, decision-making, negotiation and more in different VC firms

The most important considerations and their priorities for decision-making in different VC firms

A good company and a good deal, what’s the difference?

The involvement and exit strategies after investing in startups

The prioritized innovations/solutions you are looking for from startups now

Advice for deep tech startups to build a relationship with you as well as fundraising preparations

Whether you are an entrepreneur or an angel investor, if you are interested in joining the conversation, and asking your questions to the panelists, including feedback on your startup, market insights, etc., sign up here. This is an invitation-only event. If you sign up, you can ask questions, and no matter whether you join or not, we’ll send you the meeting summary.

Speakers

Alexander Hall-Daniels – Alex is a program manager and had been a senior analyst with SOSV IndieBio’s New York office, a VC investment firm operating within biotechnology and life sciences. He has a diverse, global perspective cultivated from the wealth of international professional and educational experiences across the US, UK, and the rest of Europe.

Mike Huang – Mike is an investment manager with Lam Capital (Lam Research CVC), focusing on semiconductor manufacturing startup investments now. previously he has worked with Amazon, Samsung Electronics, and TSMC. He has an educational background in technology management and MBA from Taiwan and UK.

Yvonne Chen – Yvonne has over 20 years of success in telecom, security, MedTech, and early-stage investments and operations, including handling corporate investments at MICROELECTRONICS TECHNOLOGY INC., CDIB & PARTNERS INVESTMENT HOLDING CORP., H&Q TAIWAN CO., HTC CORPORATION, WI Harper, and Infinity Ventures. She has strong industry expertise and connections in Taiwan, Greater China, and Silicon Valley.

Jessie Chuang – Jessie is a startup advisor with US and international teams, a judge with Unicorn Battle and MassChallenge, an angel investor with several US angel networks, and an emerging venture fund manager. Her previous experience includes 10+ years in semiconductor R&D and team management at UMC, and another 10+ years in corporate consulting on digital transformation working with executives.

About TINVA

TINVA (Taiwan ITRI New Venture Association) is a Non-Profit Organization startup facilitator and venture builder that partners with various deep-tech stakeholders in order to provide startups with the resources, mentors, tools, and support needed in order to succeed. TINVA is associated with the top deep-tech research institute ITRI backed by the Taiwan government – the top source of deep-tech startups and innovations in Taiwan.

About Global League

Global League is an investor partnership with augmented collective intelligence built from a process proven by top angel networks with an average IRR >25% and 330+ exits. We connect quality investment opportunities from top US angel networks and VCs and collect intelligence from co-investing fellows.

About Founder Institute

The Founder Institute is the world’s most proven network to turn ideas into fundable startups, and startups into global businesses. Since 2009, our structured accelerator programs have helped over 7,000 entrepreneurs raise over $1.75BN in funding. Based in Silicon Valley and with chapters across 100 countries, our mission is to empower communities of talented and motivated people to build impactful technology companies worldwide.

About Wise Ocean

Wise Ocean builds up a global network to connect proven startups or scaleups, industry leaders, corporate innovators, ecosystem partners, and investors for impact and profit-making. For international startups entering the US market, we will help navigate US resources (partners or accelerators) matched to your needs, for US companies looking for Asia manufacturing or market partners, we have several partners that can help, such as TINVA.

Early-stage investors are often long-term partners of startups. Angel investors usually write first checks to entrepreneurs before venture capitalists can commit. Beyond funding, angels can be mentors/advisors for founders. They are usually high-net-worth individuals with industry experience and connections, who can open doors (make introductions) for startups. There are different kinds of angel groups. In this panel, angel investors from Taiwan, Singapore, Indonesia, and the US will share their experience in angel investing and how they evaluate, invest and help startups. (panel talking in English, Chinese briefing will be provided)

Introduction to angels and angel networks / 天使投資人和天使網絡有哪些不同類型?

How to find angel investors that are good partners for your startups? / 如何找到合適的天使投資人?

How to raise funding from angel investors? / 如何向天使投資人募資?

How do angel investors evaluate and invest in startups? / 天使投資人如何評估創業公司並進行投資?

How might angel investors help and support entrepreneurs? / 天使投資人可能如何幫助創業團隊?

What do you observe in the current angel investing climate? / 現在市場的天使投資與早期投資有何趨勢?

What do angels expect to get from investing and supporting startups? / 天使投資人為何要投資與幫助創業團隊?

What angel groups have created an average IRR > 25%? / 那些天使投資社群創造了平均 IRR > 25% 的成績?

What are the secret sauce of successful angel networks? / 成功的天使投資社群有何秘訣?

What are angel investors looking for in 2023? / 今年(2023) 天使投資人在找什麼投資標的?

Introduction of Taiwan ITRI New Venture Association(台灣工研新創協會)、Central Texas Angel Network(美國)、Bali Investment Club(印度尼西亞)、Taiwan Global Angels。

Whether you are an entrepreneur or an angel investor, if you are interested in joining the conversation, and asking your questions to the panelists, including feedback on your startup, market insights, etc., sign up here. This is an invitation-only event. If you sign up, you can ask questions, and no matter whether you join or not, we’ll send you the meeting summary. 無論是創業者或天使投資人,都可以報名參加,跟這次會談者提問交流。只有報名取得會議邀請才能參加。如果你報名,無論是否參加,都可提問,我們會後將寄送會談重點摘要。

Speakers

Bryan Huang – Bryan is the Managing Partner of TaipeiLaw Attorney-at-Law and Co-founder of Taiwan Global Angels. He is a legal advisor for investment in China, Taiwan, and States with broad experience in all aspects of startup and venture capital, accounting, tax, and financial management. He is passionate about connecting Taiwan with the global community.

Joseph Liu – Joseph is a member of 3 angel networks, Central Texas Angel Network (CTAN), Tech Coast Angels (TCA), and Chemical Angel Network (CAN). He is a board director of CTAN. His investment portfolio is comprised of companies across Life Sciences, B2B Software, Hardware, and CPG industries. He has 5 exits and 30+ active companies in his portfolio. Joseph is working with Jessie on venture investment.

Michelle Kung – As the Chairman of the TINVA Singapore Chapter, she is currently assisting leading technology companies from Taiwan to enter into SEA markets through venture building, international funding, local market partnership, and governmental support. Michelle is an investor in tech start-ups in SEA and Europe. In addition to funding support, she continues engaging with the regional start-up ecosystem as a mentor/advisor/judge for start-ups and partners.

Tom Courly – Previously in management consulting, focussing on digital innovation and agile transformation, Tom now develops Indonesia’s Start-Up landscape, building the impact-driven venture giants of tomorrow with Bali Investment Club, angels, and founders. Tom is also a Strategic Advisor and Commissioner for many of BIC’s current and upcoming portfolio companies.

Jessie Chuang – Jessie is a startup mentor working with US and Taiwan teams, a partner at Network VC, a judge with Unicorn Battle and MassChallenge, and an angel investor with several US angel networks, and an emerging venture fund manager. Her previous experience includes 10+ years in semiconductor R&D and team management at UMC, and another 10+ years in corporate consulting on digital transformation working with executives.

About Foundersbecker

Foundersbacker is a unicorn factory in the circular economy industry. In other words, Founderbacker is an ecosystem builder focusing on the circular economy of food, cloth, and shelter; we call ourselves “Xiaomi in circular economy!”

About TaipeiLaw Attorney-at-Law

TaipeiLaw Attorney-at-Law stands with entrepreneurs and offers professional advice and effective strategies that do not backfire. We support clients on legal battlefields amid market competition. Our team includes attorneys and accountants fluent in Chinese, English and Japanese.

About TINVA

TINVA (Taiwan ITRI New Venture Association) is a Non-Profit Organization startup facilitator and venture builder that partners with various deep-tech stakeholders in order to provide startups with the resources, mentors, tools, and support needed in order to succeed. TINVA is associated with the top deep-tech research institute ITRI backed by the Taiwan government – the top source of deep-tech startups and innovations in Taiwan.

About Wise Ocean

Wise Ocean builds up a global network to connect proven startups or scaleups, industry leaders, corporate innovators, ecosystem partners, and investors for impact and profit-making. We are also building the Global League fellowship with global-minded investors for global collaboration.

About Founder Institute

The Founder Institute is the world’s most proven network to turn ideas into fundable startups, and startups into global businesses. Since 2009, our structured accelerator programs have helped over 7,000 entrepreneurs raise over $1.75BN in funding. Based in Silicon Valley and with chapters across 100 countries, our mission is to empower communities of talented and motivated people to build impactful technology companies worldwide.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.