The investor panel recording on the agri-food topic (Jan.19, 2024), and here is Transcription by Swell.ai.

Thanks to all the panelists for the great conversation and the Chat record is here.

Our special guest Thomas Mastrobuoni, CIO of Big Idea Ventures (BIV), shared sincerely about the agri-food tech ventures from his experience with BIV and Tyson Ventures. BIV has invested in more than 110 food tech startups. Before BIV, Thomas worked with Tyson Ventures for about 3 years, launching and running their corporate venture capital group. It was the first CVC group for Tyson with a $150 million mandate from the company to invest across both enabling technologies, but also disruptive technologies, which led to investments not only in things like rapid pathogen detection and direct-to-consumer platforms but in alternative proteins as well, both on the plant-based side and on the cultivated or cell-based side.

Their latest fund is a new model, according to Thomas (lightly edited for clarity):

We call it the Generation Food Rural Partners Fund, or GFRP. This fund is very different than the new protein fund strategy. This fund works for solving problems in the supply chain for food and agriculture companies. So we will talk to the Nestle’s, we’ll talk to Unilever, all the way down to a small stakeholder farmer, here in the States and in Europe. And we’ve built basically a data lake of problems that these folks are trying to solve, whether it’s around single-use plastics, scaffolding for cultivated proteins, replacement for petroleum-based adhesives. We map the universe of problems as well as we can. And then we work back to a pool of university-developed research and IP. And the goal is to start around 20 to 40, depending on how big the fund gets, but 20 to 40 new companies based on baskets of university IP, so not one patent, but multiple patents, coupled with experienced management teams to build companies to solve some of these problems that these companies are trying to face, which are the reasons why none of them are going to hit their GHG reduction goals in time.

This fund is also a licensed RBIC fund. RBIC stands for Rural Business Investment Company. It’s a license issued by the USDA, very similar to SBIC funds. It’s a license that allows banks to invest in our fund. Any other LP can invest in our fund. Typically banks cannot invest in private funds due to the Volcker rule, but SBIC licenses and RBIC licenses are exemptions to that. So we launched our fund with 10 farm credit banks.

So if you’re a farmer in the US, you bank at farm credit, your mortgage is with them, your tractor leases are with them, etc. They have a mandate to drive economic growth and development in rural communities. And they do that with us by committing LP capital to our fund. And we spin up new companies, as I said, to solve these supply chain problems. And we put our new companies and the living wage jobs we create in rural communities to drive that economic growth and development. Our areas of focus are food, protein, and agriculture. We’re purposely broad.

Tom shared their summary on interest areas in demand from talking with corporate partners and LPs – read the breakdown here.

Below is our writing about the context of the agri-food system.

The Agri-Food Industry can become net-positive

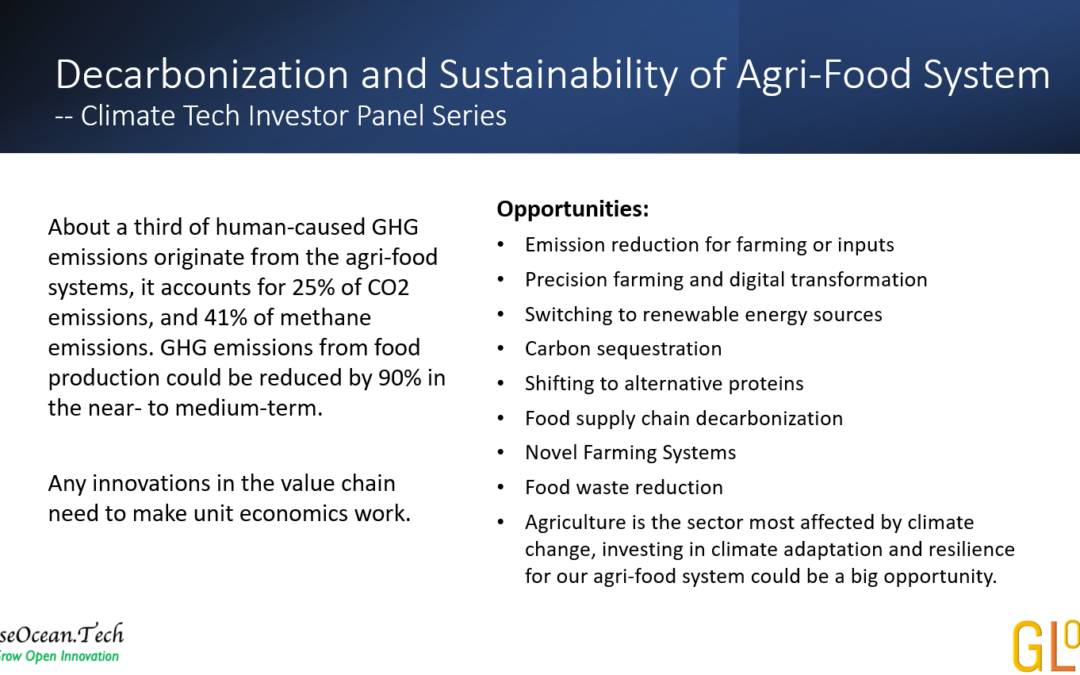

About a third of human-caused GHG emissions originate from the world’s agri-food systems (source), it accounts for 25% of global CO2 emissions (source), and 41% of global methane emissions (source). This scale has driven significant investments in decarbonization along the value chain. Declaration on Sustainable Agriculture, Resilient Food Systems, and Climate Actions was announced on 1 December at COP28 and was endorsed by 134 heads of state and government. Unlike some other hard-to-abate sectors, the food industry can play an important role in the net-zero transformation since it has the opportunity to become net-positive, by achieving net zero and acting as a carbon sink for other sectors.

On the other hand, agriculture is the sector most affected by climate change according to the UN Food and Agriculture Organization. Over the last 3 decades, agriculture losses accounted for an average of 23% of the total impact of disasters across all sectors. Climate change is accelerating land degradation and making it harder for food systems to adapt, posing significant threats to food producers. This can include both workers and working conditions impacted by extreme weather. Regarding agriculture, only five countries have benefited from climate change, while 21% of overall global agriculture productivity has been lost (source). Investing in climate adaptation and resilience for our agri-food system could be a massive opportunity.

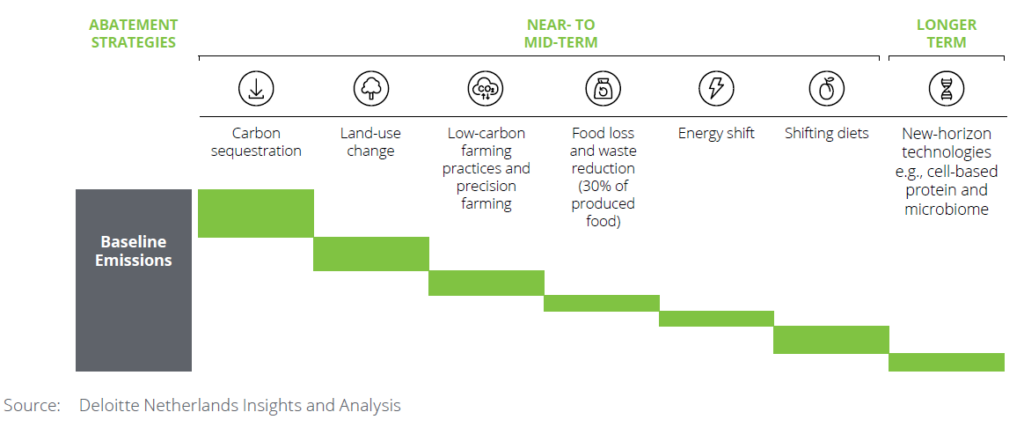

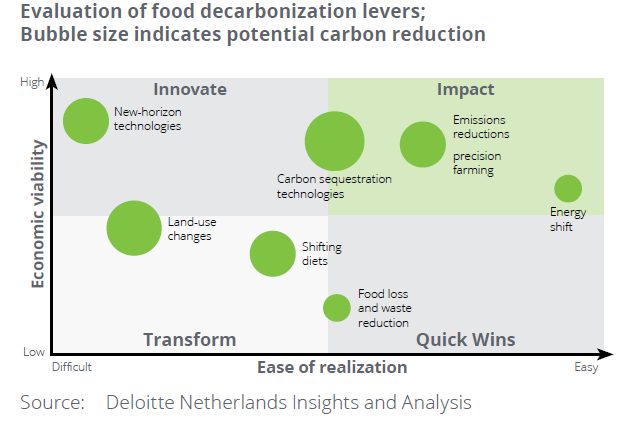

Implementing these decarbonization levers will require significant financial investment and change management across the food ecosystem. Except for food loss and waste reduction, there are no quick wins. From the Deloitte report, this chart depicts the economic viability and ease of realization of those levers, those levers falling in high economic viability and high ease of realization are more likely to make bigger impacts in the shorter term.

Emission reduction for farming or inputs can greatly reduce both CO2 and methane emissions. Rice and livestock are the main emitters of methane in agriculture. There are opportunities to drive on-farm decarbonization or reduce applications of inputs (fertilizers, pesticides, etc.) and capture business value. Decarbonizing those inputs matters too. And, new bio methods are emerging to reduce enteric emissions in livestock such as methane vaccines, etc.

Precision farming and digital transformation can make food production more sustainable. Digital management software, data analytics and AI, sensing technologies, robotics, electrified equipment, carbon monitoring, digital marketplaces, etc. can support data-driven decision-making in farming and demand forecasting, reduce labor needs, level up operational efficiency (faster response or automation, higher crop yield, better animal health), reduce chemical inputs, and water use, and reduce waste.

Switching to renewable energy sources to power food production and distribution can lower emissions. The food sector could also produce energy from waste using devices like bioreactors. Anaerobic digestion can turn organic matter into electricity, heat, or renewable natural gas or fuels.

Carbon sequestration can remove carbon from the atmosphere. For example, changing the way of treating soil can contribute greatly to emission reductions. Increasing the organic matter – and therefore the carbon stored – in soils can be done in a variety of ways, such as applying compost, biochar, or organic fertilizer. Some methods can make sure carbon stays in the soil. Agroforestry, which combines agriculture with the carbon storage capabilities of forests, is another promising option.

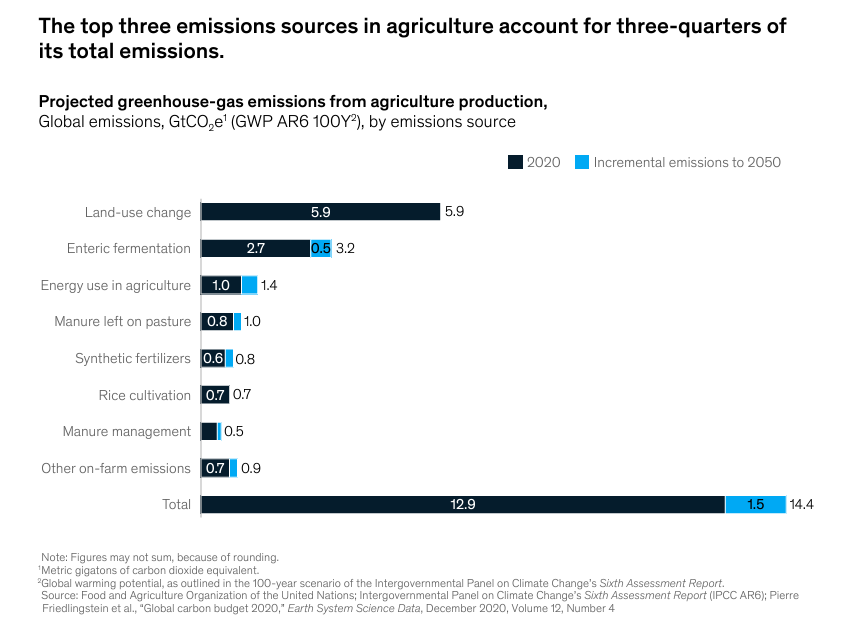

From McKinsey’s report: The agricultural transition: Building a sustainable future (June 2023): a wide variety of emissions sources are associated with agriculture; however, three major sources combined account for nearly 74 percent of the total, making them excellent targets for action – land use change, enteric fermentation, energy use in agriculture. (image below)

Agriculture alone is estimated to account for approximately 80 percent of global land-use change, which profoundly impacts carbon release and negatively affects biodiversity and ecosystems. Agricultural land covers half of all habitable land and is responsible for 70 percent of freshwater withdrawals. In addition, food systems are the primary driver of biodiversity loss around the world. Restoration and conservation are the most effective levers for abating land-use emissions, in addition to others including integrated farming systems such as Silvopasture, agroforestry and agrovoltaics. Carbon and nature markets today are supporting farmers in adopting nature-based solutions such as cover cropping and no-till farming, for which they can generate and sell carbon credits. The Inflation Reduction Act in the United States includes $5 billion specifically for climate-smart forestry and wildlife protections.

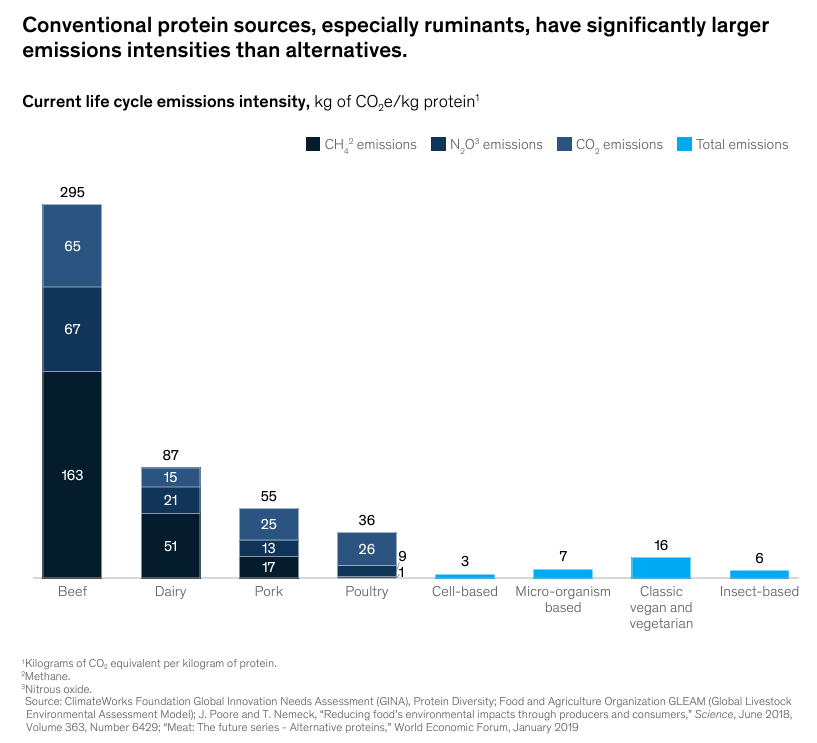

Shifting what we eat to alternative proteins is a powerful lever for at least 2 reasons. First, no methane emissions from livestock. These methane emissions increase atmospheric temperature approximately 80 times more than CO2 on a 20-year outlook, but methane has a shorter atmospheric lifetime than other GHGs, making it an effective target for reducing global temperatures quickly. Adopting alternative proteins, including classic plant-based products and precision-fermented and cellular products can avoid a substantial amount of emissions, and they have much smaller physical footprints (comparison as below, dietary shifts away from animal proteins could save nearly 640 million hectares of land, McKinsey pointed out) and consequently limit future land conversion while creating opportunities for sequestration.

Public funding for alternative proteins increased significantly, with governments worldwide more than doubling their investments in 2022 alone. As a result, all-time public support for the alternative protein ecosystem has likely surpassed $1 billion. In 2023 Upside Foods getting regulatory approval to sell their cultivated chicken in the US is a breakthrough. Policies can support consumer adoption of alternative proteins. This report from Good Food Institute tracks the investment, support, and regulation enacted across the globe. The shift to alternatives needs to be led by wealthier nations, they can afford such solutions. Developing nations could focus on enhancing animal productivity.

Food supply chain decarbonization includes smart packaging and supply chain efficiency measures that can reduce raw material consumption and the distance food needs to travel. Using bioplastics packaging or recycled packages can reduce emissions, Coca-Cola and 8 bottling partners created a fund focusing on this (source).

Novel Farming Systems, as the AgFunder-defined, include indoor crop farming systems such as vertical farms and greenhouses, insect ag, aquaculture, and algae production. There are very interesting big deals that happened in the Agriculture and Food sector in 2023.

From farm to fork, some innovations are happening closer to the fork side, such as digital food management, food waste reduction, traceability technologies, food safety solutions, 3D food printers, consumer engagement, etc.

Any innovations in the value chain need to make unit economics work. Most foods are commodities and farmers usually have thin margins, new offerings can’t transfer costs to the customers or downstream partners. And, startups can not play heavy Capex games, and might need to partner with big companies with a lot of cash, could offer offtake agreements or even operational agreements where they’re going to run the factory.

CTVC reported: that in 2023, the total funding in climate tech is $32B, a 30% drop YOY, while CAGR remains high since 2020 at 23%. Transportation and Energy investment declined but remained on top. Food & Land Use fell dramatically, down -55%, and was replaced by Industry in the big three. But, according to Pitchbook’s reporting, AgTech is the only sector with a median valuation held up +10% YOY, even better than the AI/ML sector. Is this a good time for investors to participate in the long-term trend? What are the solid trends and opportunities in this downturn stress test? What startups are moving the needle for the industry forward?

This Friday (Jan. 19, 2024), we’ve invited Tom Mastrobuoni, the Chief Investment Officer at Big Idea Ventures (BIV) to join our chat. Big Idea Ventures, with offices in New York, Paris, and Singapore, is the world’s most active investor in FoodTech and AgTech and has invested in 110 companies across 25 countries. The company has contributed to the development of the growing alternative protein industry since its inception. BIV is backed by a network of strategic partners including AAK, Avril, Bühler, Givaudan, Temasek Holdings, and Tyson Ventures, and is partnering with governments around the world working on food security and new food ecosystems. Take a look at their 2024 outlook: The Way Forward for Agri-FoodTech in 2024.

To join our chat on the ClimateTech Investor Panel, sign up here if you’ve not done so. Introducing yourself is welcome.

Note: Our panels/meetings aren’t for startups to pitch, but startups are welcome to share industry insights, and investors are welcome to introduce outstanding startups or funds. The goal is to discover trends and great startups or funds.

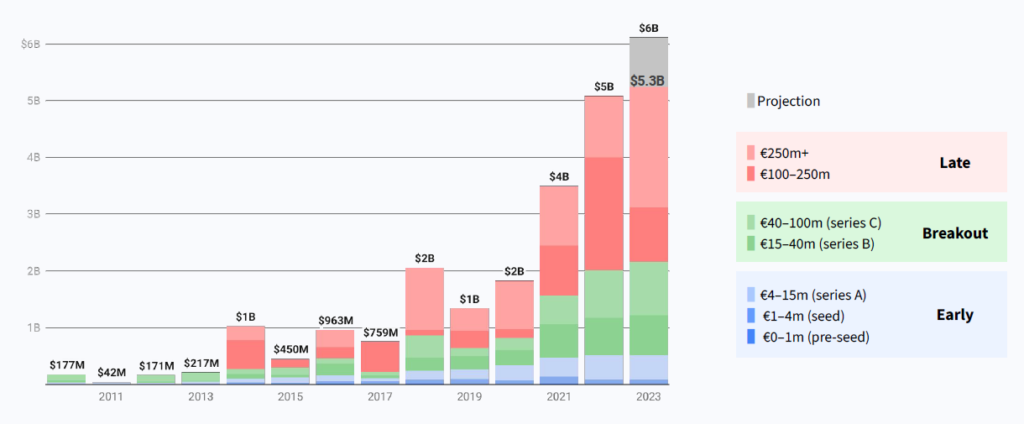

Green Building Startup Investments at Record High in 2023

Global investment in clean energy had been on track to reach an all-time high in 2023 – $1.8T – according to IEA, $500 billion more than in 2022. And one of the agreements from COP28 is a commitment to triple the world’s capacity of wind, solar, and other renewable energy by 2030, concurrent with a doubling of the pace of energy efficiency gains. Although VC investments in climate tech decreased almost 40% YoY like the general trend, VC funding into green buildings had the best year ever in 2023 according to a report published by 2150 and Dealroom in 2023 November – Funding for green building startups is already at record high levels with $5.3B in 2023, projected to grow over 3x in respect to 2020, as below.

Chart from Urban Tech 2023 by 2150 and Dealroom (data as of 2023 November)

Policies

Policies worldwide are accelerating the transition to more sustainable cities with focus on building energy efficiency, heating and cooling.

The building sector is responsible for over 1/3 of total greenhouse gas emissions in Europe. Residential heating, in particular, accounts for the largest share of GHG emissions in buildings. The EU has now revised its Energy Performance of Buildings Directive (EPBD) and the Energy Efficiency Directive (EED) to transform the EU’s building stock as a main decarbonization lever. There are 4 key measures: (1) Energy Performance Certificates (EPCS), (2) Minimum Energy Performance Standards (MEPS), (3) Zero emissions buildings (ZEBS) – All buildings will have to receive a label D by 2033 and A by 2050. (4) Low Carbon District Heating – phase out fossil fuel heating by 2040.

In the United States, California passed a first-in-the-nation embodied carbon code for commercial buildings and schools (that RMI helped shape). New York became the first state to legislatively require all new buildings to be electric. In 25 US states, governors committed to installing 20 million heat pumps by 2030. Washington State passed building codes that will require new homes to provide energy-efficient heating and cooling. And Massachusetts passed a first-in-the-nation ruling that puts the state on a faster path to electrify heating.

New York City:

In New York City, Local Law 97 (LL97) imposes carbon caps and reductions on buildings larger than 25k square feet. Affordable Housing Buildings that include affordable and rent-regulated housing are not exempt from the requirements of Local Law 97, but they may be treated differently. Many components of the bill will be phased in gradually beginning in 2024. Carbon restrictions will be tightened during a series of compliance periods until 2049. By 2050, all buildings must meet zero-emissions standards.

Opportunities

Planet A Ventures pointed out these opportunities are noteworthy: (1) Digital tools for life-cycle energy audits of buildings, (2) Technologies and service providers for renovations, (3) Technologies for recycling and low-carbon materials, (4) Technologies for low-carbon heating.

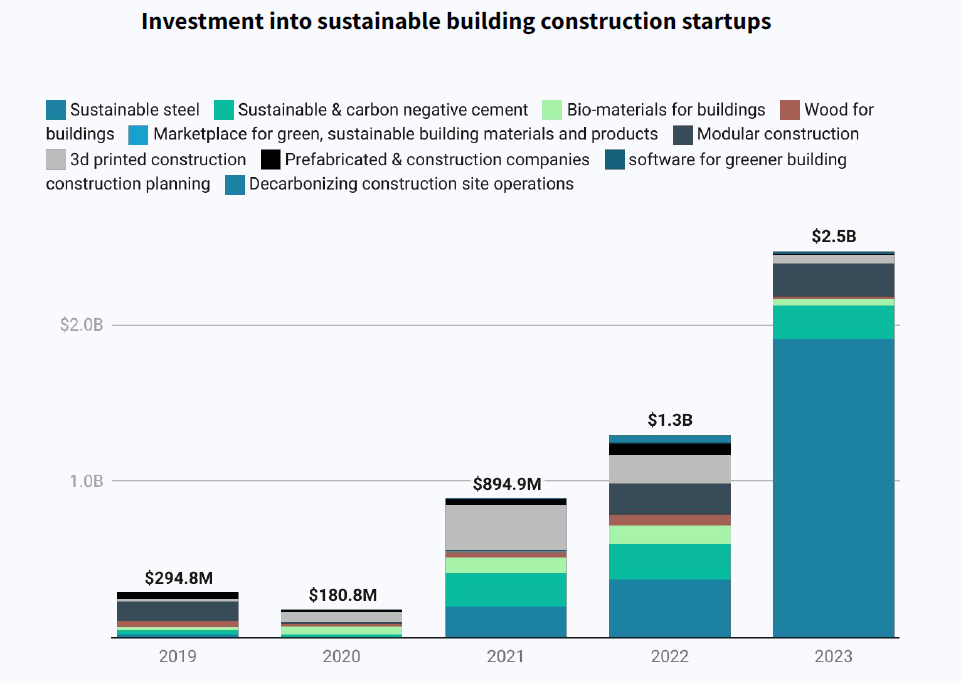

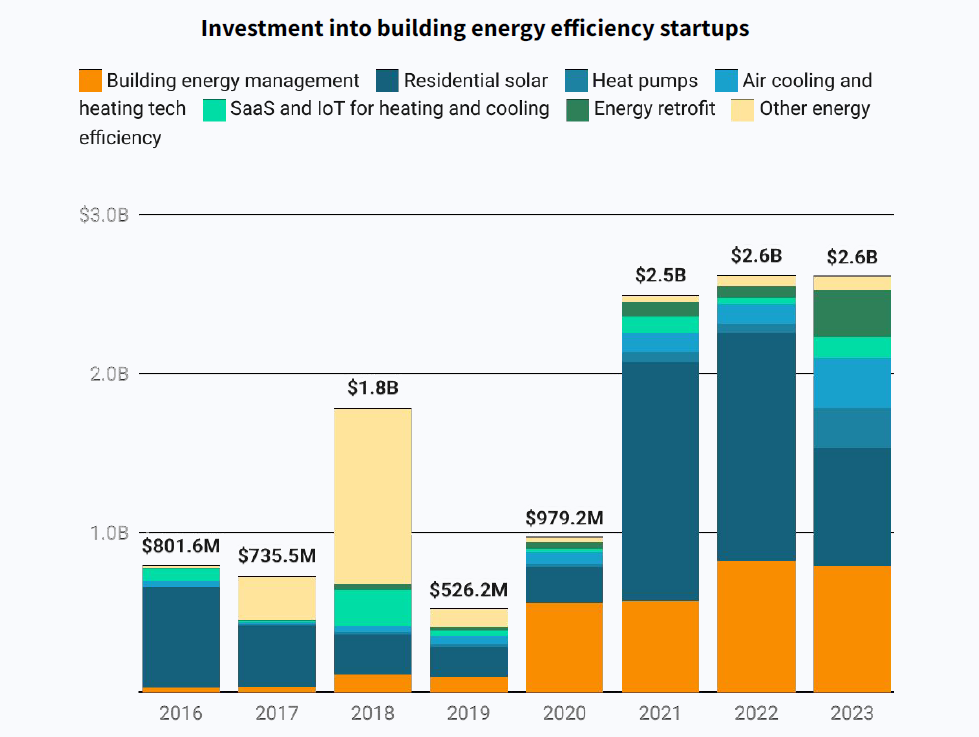

In the Urban Tech report from 2150 and Dealroom, it’s highlighted that the biggest subcategories (in terms of funding) of Urban Tech unicorns are sustainable building construction and building energy efficiency companies. VC funding in both subcategories had kept growing in 2023 despite of the cooled VC investments. Overall there are 4 subcategories summarized in the report; enable, experience, build, and operate.

Enable: SaaS x construction startups have suffered a whopping 68% decline in VC funding despite the construction industry productivity challenges. VC funding for construction SaaS startups peaked in 2021.

Experience: Driven by real-world events, startups aiming to prevent and combat wildfires have raised over $100M in VC funding, on par with 2021 records, and grown 7x since 2018.

Build (planning, materials, construction, and processes): Sustainable building construction startups have raised a record $2.5B in 2023, far more than ever before, driven by materials innovation such as sustainable cement and green steel.

Source: Dealroom

Operate (sensors and platforms to monitor, manage, retrofit, and optimize buildings and energy efficiency): Building operation decarbonization startups had their best year with $2.6 already raised, on track for a record of over $3B, led by building energy management and residential solar. Heat pumps and energy retrofits have also shown strong growth.

Source: Dealroom

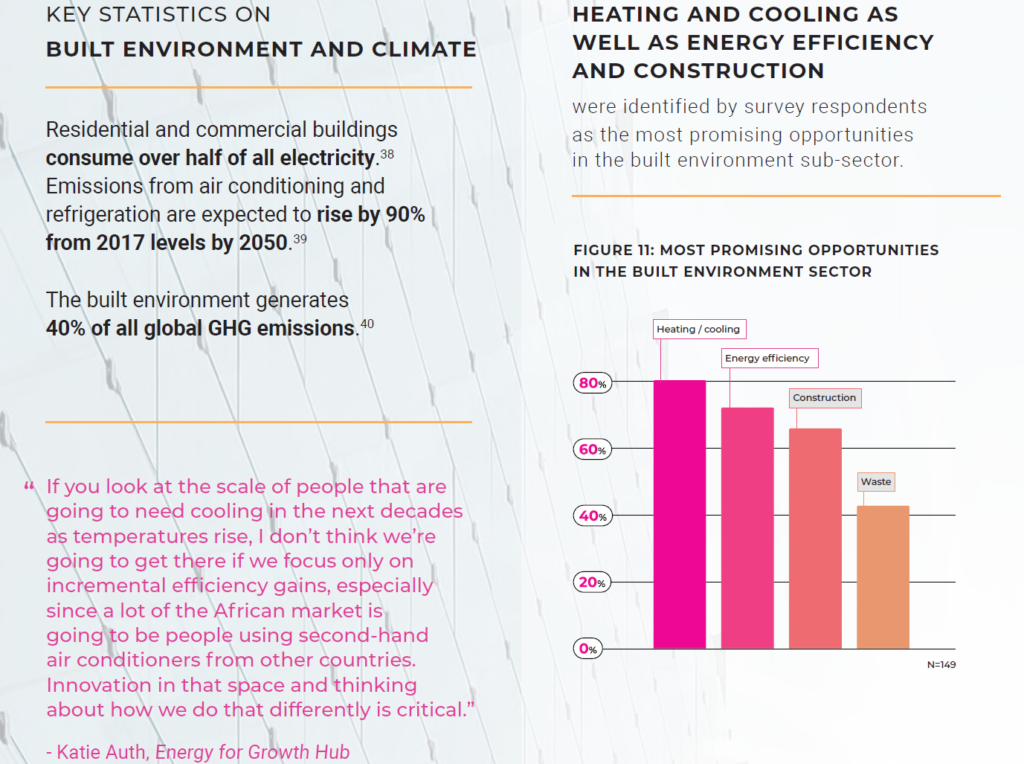

According to Oxford Climate Initiative’s report, the top 3 opportunities in the built environment are (1) Heating and cooling, (2) Energy efficiency, (3) Construction.

Image from the Oxford Climate Tech Initiaitve 2023 report

In 2023 September, a consortium of US states and territories representing more than half of the US economy announced a commitment to collectively reach 20 million residential electric heat pump installations by 2030. At least 40 percent of benefits flow to disadvantaged communities. (more on RMI) In 2023 November, the U.S. Department of Energy (DOE) announced a historic $169 million for nine projects to accelerate electric heat pump manufacturing at 15 sites across the US. The selected projects are the first awards from DOE’s authorization, invoked by President Biden using emergency authority on the basis of climate change, to utilize the Defense Production Act (DPA) to increase domestic production of five key clean energy technologies, including electric heat pumps.

Heat recovery/reuse is another opportunity. Some cities have built underground networks that can reuse heat from facilities like industries, data centers, and wastewater treatment centers to heat other buildings and tap water. These cross-sector heat recovery systems, are called heat networks. (read more) Furthermore, cooling is expected to be a significant contributor to energy use in the future, foreseen to triple in demand globally by 2050. Through COP28 over 60 countries signed up to a so-called ‘cooling pledge’ with commitments to reduce the climate impact of the cooling sector, which could also provide “universal access to life-saving cooling, take the pressure off energy grids and save trillions of dollars by 2050.” At the same time, conventional cooling, such as air conditioning, is a major driver of climate change, responsible for over seven percent of global greenhouse gas emissions. (more on UNEP-led ‘Cool Coalition’)

Any tech that helps with the coordination of dynamic energy flows and the efficiency of buildings is needed. A new market and exciting opportunity for real estate and construction is playing in the energy sector! While the energy transition discussion often focuses on the utility-scale transition, the spotlight is growing on the critical role of a lower-cost, lower risk approach which puts buildings and the building sector front and center.

Consumer Energy Resources is an area of untapped opportunity that will continue its growth trajectory in coming years, encouraged by high grid prices. The ongoing high uptake of solar and batteries should see the capital costs of these technologies continue to decline. With that will also come a higher uptake of enabling technologies like smart meters, and smart devices that help with efficiency.

All of this represents an exciting opportunity for the building and construction sector to use its skills, services, and assets. Our industry, across all tiers, will increasingly be required to enable this ongoing customer-led transition. Where once the distribution companies held out against the two-way flows of electricity and the advent of “Prosumers” – those of us who generate more than we need – governments and electricity industry captains now have a sense of the opportunity that comes with being at the heart of this transition, and they need our help. More importantly, the time isn’t coming, it’s here.

We also reached out to Canada’s largest climate tech seed fund – Active Impact Investment. One of their theses is “Adapting and monitoring the built environment to efficiently use energy and other resources without sacrificing services.” One investable whitespace they highlight:

As the demand for clean energy grows, we see exciting investment opportunities in software and sensors to support the transition: a 60GW virtual power plant (VPP) could meet future resource needs at a net cost $15-35B lower than the cost of new generation. VPPs connect multiple energy generation and consumption assets in real-time to shape the electricity load—saving energy costs by 40-60% while increasing grid resilience.

We continue to see opportunities in energy retrofits and automation systems, which can save 10-40% in energy costs and are expected to be a $273B market by 2032. We also see investable whitespace in companies that create efficient extraction techniques and reuse systems for precious metals–which will require $250-$350B in capital expenditure by 2030 to support the growing demand for renewables, energy storage, and EVs.

As Active Impact Investment pointed out: “39% of global emissions come from construction & the built environment, 30% of the energy used by buildings is wasted. Between 2015 and 2020, power outages had increased 60% due to grid unreliability.” There are big opportunities behind decarbonization and sustainability of our built environment.

On Jan. 12, 2024, our ClimateTech Investor Panelwill invite/welcome investors, industry experts, and entrepreneurs to have a discussion on this topic. We’ve invited Zohaib Dar, Consultant of EY specializing in energy transition and digital transformation of built environments with first-hand experience with corporate venture and innovation programs, and Jessie Chuang the coordinator of Global League, to moderate the discussion. Everyone can introduce themselves, we love to see a more interactive networking and exchange event. (Learn more about Global League)

Questions to discuss:

What are investors looking for (investable whitespace)? Which sub-sectors of the built environment have the most promising potential or are underinvested? What sub-sectors are too crowded?

How do investors identify and evaluate investments?

How about policies and incentives that encourage or mandate the adoption of low-carbon technologies and practices, such as carbon taxes, subsidies, standards, and credits?

What are the risk factors of investing in this built or urban tech space? How could we help de-risk them?

Introductions of promising innovations and startups (by investors or advisors)

As diversified clean energy sources are being built, how to orchestrate different and distributed energy sources? The biggest challenge in the energy transition could be the infrastructure supporting the transition of electrifying everything. This topic is prioritized in our panel planning before we dive into other sub-sectors, related topics include VPP (Virtual Power Plant), V2X (EV battery as an energy storage/source), DER (Distributed Energy Resources), grid optimization, etc. We found recent news speaks the same priority. From Pitchbook’s Q3 2023 Clean Energy Report, the grid infrastructure segment received the highest VC funding in Q3 2023, with 41.5% of total deal value for the quarter. Insight Partners also identified “Grid decarbonization and optimization” as the very top opportunity among the 4 promising areas of climate tech investments (the writing is here).

For the whole picture, new infrastructure establishments also include other elements beyond grids – data, governance, community, financing, portfolio building and integration. Texas, the epic center of climate tech innovations, is an interesting example to discuss. Not only does Texas have its own system and governance, but everything is bigger in Texas, including its electricity use, which is increasing at historic rates in a sign of what is to come for much of the U.S. The country’s largest electricity producer and user saw sales growing at five times the national rate for the past decade! (according to Wall Street Journal) The solar and wind energy scales in Texas are both number one in the nation, and Texas has started to pilot ADER with the Tesla Powerwall. We invite a founding member of CleanTX, Thomas Ortman, an energy industry executive and technologist, to share his insights on a clean and optimized grid. The scope is beyond Texas.

To look at this topic from an investor’s lens, we invite Bob Bridge, the founder of SWAN Impact Network and co-founder of the Semilla Climate fund. He said — There are a diverse set of players contributing to the energy transition: federal and state governments, grid operators and regulators, established multi-national and national system vendors, installation and service companies, manufacturing companies, technology startup companies, universities, and more. Each player plays a different role. Where are the most interesting opportunities for startup companies and their investors?

Speaker

Bob Bridge, Founder of SWAN Impact Network and Co-founder of the Semilla Climate Fund – Bob has extensive experience in founding and taking early-stage technology start-up companies to successful exits, having been in startups that returned $430M to investors, and previously raised $60M for the companies that he founded. He had served as a VP and General Manager of a division of a public company.

Thomas Ortman, President of Nous Energy and Founding Partner of CleanTX Foundation – Thomas has forty years in the engineering design and build sector with electro-mechanical engineering design expertise in electronics, clean technology & semiconductor products, and capital equipment experience. He founded Concurrent Design, Inc. which led to a merger with Voltabox of Texas, Inc., and he turned into CTO of Voltabox of Texas.

Host: Jessie Chuang – Jessie is a deep tech startup advisor and investor, and the managing partner ofGlobal League – a vetted network for accredited/professional investors to collaborate on deal evaluation and syndication, to identify and help the most impactful ventures. Her previous experience includes semiconductor frontier R&D management and global consulting on digital transformation and AI.

About CleanTX Foundation – CleanTX is an economic development and professional association for CleanTech and renewable energy businesses. Its mission is to modernize the power grid to advance renewable integration through industry collaboration and strategic alliances through chapters throughout Texas. Its vision is to achieve 50% renewable energy integration in ERCOT by 2030.

About SWAN Impact Network – SWAN is a 501(c)(3) non-profit with a network of angel investors focused on investing in companies that aim to deliver measurable social or environmental impact, and who also have solid plans for financial success.

About ClimateTech Investor Panels – This is for accredited private equity angel investors, venture capitalists, and corporate/institutional investors to share insights and investment opportunities and catalyze collaboration to help ClimateTech startups.

I spent a lot of years in hard tech (a lot in startups and semiconductors). I always have a deep concern about our environment and people being cared for, so I created SWAN Impact Network, an angel network of 85 members, we’ve invested about 14 million in startups, a bulk of which is in climate tech. So we also put together a climate tech fund. We are very selective, and we are well-connected in the Texas climate tech community, also we have a lot of support for companies founded by underserved people.

About market opportunities, what we don’t like are – battery chemistries (too many of them, it might take 15 years for them to realize an impact), direct carbon capture technology (is interesting but not for seed companies), marketplaces for greener consumption, and companies relying on government subsidies or a low-interest rate. What do we like? We like industrial or commercial applications, for example, reducing carbon emissions at the sources, increasing energy efficiency in buildings or factories, more cost-effective ways to treat water, and treating pollution. We prefer companies that don’t require a lot of Capex by users.

ERCOT in Texas allows new energy generation to come out (to users) even if there is no transmission capacity to move that electricity around – a unique situation in Texas. Companies can forecast usages, and optimize grid operations with renewables are interesting. Batteries are important, but it’s very difficult to bring a new battery with new chemistry into scale (not our interest). One of our portfolio companies installs solar panels integrated with batteries, which are doing very well and will integrate into VPP in the future.

Thomas

I spent my entire career in technology development, and new product development, including a lot of semiconductors which led us to a lot of solar and wind energy, some microgrids, and ultimately into batteries, then my company attracted interest and acquisition by the European enterprise Voltabox. I have been very active in the CleanTX Foundation for several years to promote clean energies, I also was asked to serve as EIR in Austin Technology Incubator to help startups.

What are the general megatrends of this energy transition? Humans spent 140 years to build the biggest system (of energy grids) in history, and now we are revamping it to add a lot of technologies. A lot of opportunities are about efficiency because the current grid is very inefficient. We (at Texas) designed the ERCOT grid to be able to satisfy the peak loads.

About energy storage, the largest storage medium on grids now is hydroelectric power. We also have compressed air energy storage, flywheel technology with kinetic energy storage, gravity energy storage, and superconducting magnetic energy storage (storing electricity), …… there are a lot of options.

VPP (Virtual power plants), DER (Distributed Energy Resources) and V2X are closer to reality than most people realize, worth a rigorous study for investment potential. The timing of them becoming mainstream is now! In ERCOT, we have 2 ADER piloting now which is the same thing as VPP, 8 ADERs have been authorized, in total they have megawatts of power generation on demand which are also emergency backups for any blips in the grid. This is a great opportunity that all of us can participate in, it will happen very quickly. Texas and California are very proactive in this, California also has ADER piloting. After one year through 4 seasons, it’s possible the mess participation and consumption can be opened to all. 3 years from now, people will be well aware of it, and it will become common in 5 years.

The biggest pain point in Texas is transmission, current transmission lines are fully subscribed, no more capacity for serving ever-growing peaks. So, batteries are crucial. A number screamed at me – in 2023 April, California had 700k megawatt-hours of renewable energies wasted (curtailed). Tesla has sold more than 4 million vehicles, each has a 65 kilowatts battery. If you aggregate those and make them available to the grid, that’s a greater capacity than the generation from the whole nuclear fleets in the entire U.S. The concern about extra cycles of discharging-recharging caused by participating in V2X/VPP is going away now.

Food for thought: (maybe opportunities exit)

Can we use those wasted renewable energies to produce green Hydrogen?

Current production and recycling of batteries are not very green, how can we leverage renewables?

How to motivate building owners, house owners, developers or communities to invest and participate in VPP, DER, etc.? (Economics calculation and finance engineering)

Watch the interesting conversation, questions, and answers in detail here. Thanks for the great questions, Tim, Chris, Paul and John!

Supplementary Information

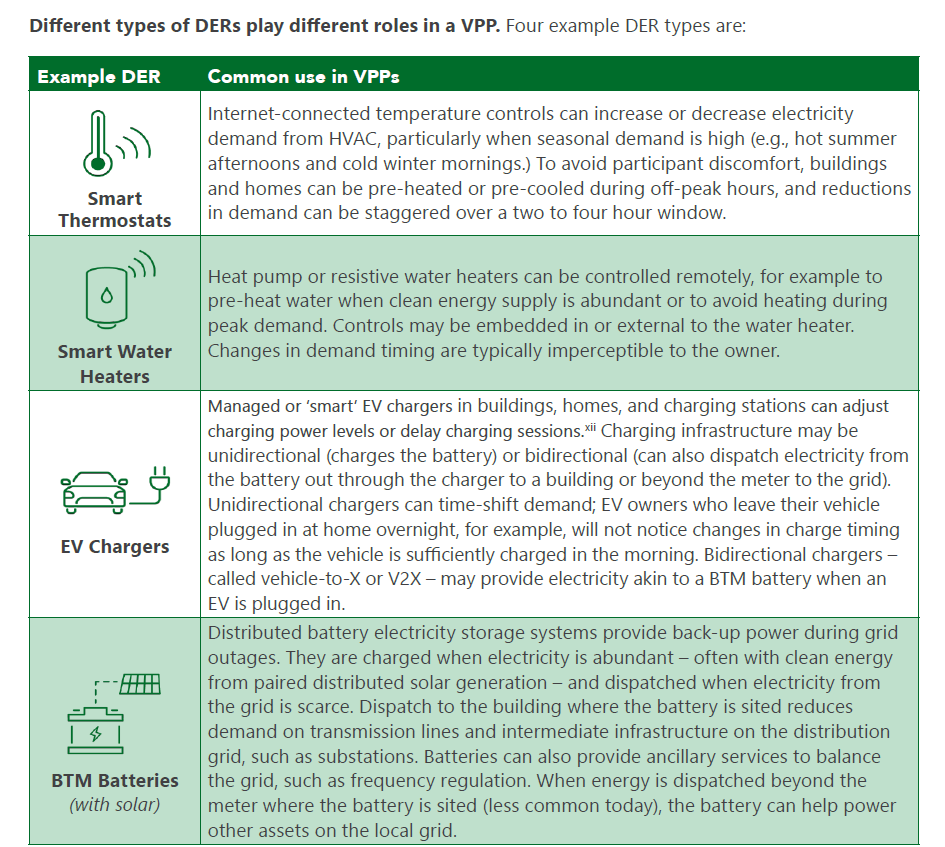

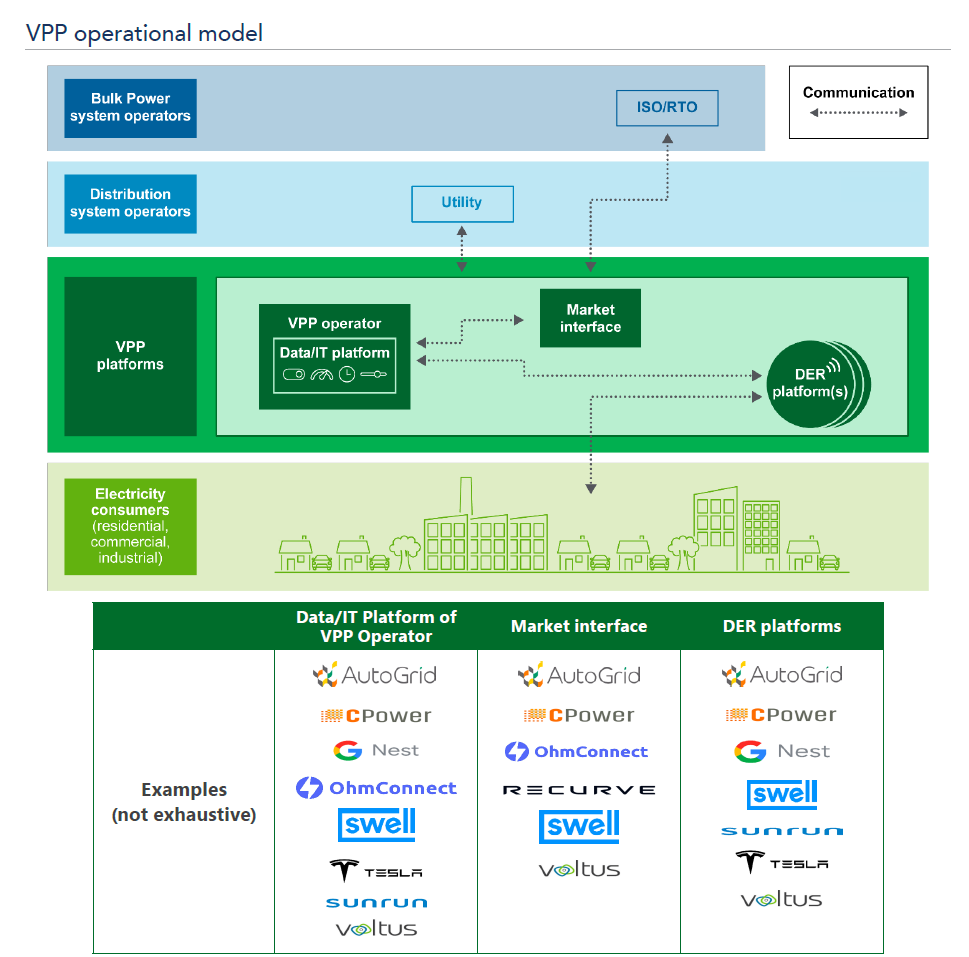

VPPs are aggregations of DERs that can balance electrical loads6 and provide utility-scale and utility-grade grid services like a traditional power plant.

DOE’s Pathways to Commercial Liftoff provides public and private sector capital allocators with a perspective as to how and when various technologies could reach full-scale commercial adoption. Check out the report about VPP. Some images from the report are used below to explain basic concepts.

What’s PACE? — The property assessed clean energy (PACE) model is an innovative mechanism for financing energy efficiency and renewable energy improvements on private property.

What’s Net Zero Energy Home? — A DOE Zero Energy Ready Home is a high-performance home that is so energy efficient that a renewable energy system could offset most or all the home’s annual energy use. Each DOE Zero Energy Ready Home meets rigorous efficiency and performance criteria found in the DOE Zero Energy Ready Home National Program Requirements.

We believe that renewable energy will only displace fossil fuels if it’s price competitive with no subsidies. For example, both onshore wind and solar energy can compete with coal, but not offshore wind. Offshore is notably more expensive than onshore which is why it’s only a small fraction of total wind energy deployed. Orsted is the global leader in offshore wind, and it has been greatly impacted by the high-interest rate now. Cost is one of the top factors that decide if a new technology or product will survive. But in climate tech, the whole context is much more complicated than usual cost numbers. That’s why we need techno-economics analysis.

Questions to discuss in this panel:

ClimateTech Adoption must make economic sense, variables including Capex, Opex, regulation penalty, government incentives, downstream markets or off-taker agreements, even carbon credits, etc., how do investors evaluate if a ClimateTech startup has attractive economic?

How to validate the cost of a new ClimateTech such as carbon capture and hydrogen storage? (technology due diligence)

How can ClimateTech startups sell to large enterprises and shorten the sales cycle?

Case studies of techno-economics analysis with climate tech startups.

Moderator

Hani Elshahawi, Managing Director of NoviDigiTech – Hani is a thought leader in the energy industry, he has more than three decades of experience (18 years in Shell) in global operations, innovation, technology management, business consulting, and the full cycle of innovation from cradle to grave and from concept to commercialization in the energy industry with roles spanning technology, engineering, marketing, business, technology, and management. Before Shell, he had worked in another leading energy enterprise Schlumberger for 12+ years.

Speaker

Amy Henry, CEO of Eunike Ventures – Amy is the CEO/Co-Founder of Eunike Ventures and Lambda Catalzer, angel investor, TiE Houston board member, principal of TiE ATX LLC (Angels of Texas), and co-founder of Texas Innovation & Entrepreneurship Foundation. Amy was named by the Houston Chronicle in 2019, “Women Who Take the Lead in Building Houston’s Tech Ecosystem” (related to the launch of Eunike Ventures). Eunike was listed in 2022 as the ‘Top 6 Accelerators/Incubators Investing in Houston’ and the ‘Top 11 Best and Most Active Accelerators in Houston. Eunike Ventures, Inc., headquartered in Houston, Texas USA is a first-of-its-kind global energy venture builder /hybrid energy technology accelerator that works with innovative, technology companies through commercialization, across the entire Energy value chain. Eunike serves a unique gap in the global innovation system by bringing together energy companies, expert talent, and best-of-breed startups.

Sujatha Kumar, CEO of Dsider – Sujatha is an entrepreneur and senior technology executive, and is the Founder and CEO of Dsider. With a background in senior management roles at multiple technology companies in the energy sector, she notably led one of them to a successful sale to Honeywell. Sujatha and her team possess extensive experience in energy and industrial markets, focusing on mid to large enterprises.

About ClimateTech Investor Panels – This is for accredited private equity angel investors, venture capitalists, and corporate/institutional investors to share insights and investment opportunities and catalyze collaboration to help ClimateTech startups.

Hani: Although cost parity is crucial for the adoption of new climate tech, the reality is much more complex. Enterprise adopters are managing a systemic change, and new tech providers need to integrate their solutions into whole systems. Techno-economic analysis needs to build assumptions, sensitivity analysis, a process model, and history matching to validate simulations with real data. Enterprises look at the lifetime value of a new investment. When I evaluate climate tech startups for investments, I need to see they have already integrated themselves into their ecosystem and clients’ systems, not just presenting a single-point solution. And if their cost structure is higher than alternatives, even mature companies might struggle when some challenges emerge (for example, high interest rate), the recent Orsted cost crisis is an example.

Sujatha: Both large enterprises and startups need to build value stream mapping, system modeling, scenario analysis, risk analysis, and transition planning for a holistic analysis and simulation before new climate tech adoptions. There is so much data involved – operational, financial, and carbon abatement data and metrics need to be integrated, also domain knowledge is needed to assist with decision-making. We help both sides to make economic sense for net zero decisions and have supported the most disruptive climate tech startups.

Amy: How startups can best engage large corporations and shorten the time to commercialization and cash generation? Many climate tech startups offer innovations in materials or chemical reactions out of labs, and there is a big gap between a proof-of-concept or prototype and a pilot. They need to be able to design a pilot to convince large enterprises and investors. To prove the business use case is economically sustainable, data and simulation are important. They will need industry veterans with experience in integrating products and services as well as with the relationships with adopters to help facilitate technology trials with process safety in mind and minimal disruption to ongoing operations. The capabilities of handling large capital projects and integration planning are required. So for investors evaluating climate tech startups, looking for qualified and experienced talents in the team or partnerships, and for due diligence, you need industry experts to get involved.

Jessie’s note:

ClimateTech might be hyped now, but the reality is complicated. This session only gives a peek into what is needed in building and evaluating climate tech ventures. On top of innovation funnels, there are too many startups that have some new breakthroughs in the labs, they need lots more resources, talents, partnerships, and ecosystem adoption readiness, besides funding, to succeed.

To get to deployment, a technology must be completely de-risked, and ecosystem economics established so that every player in the value chain has a viable economic model. This means that managing a technology portfolio solely through the well-understood and widely used Technology Readiness Levels (TRL) stage gates is not enough.

Often, commercialization fails not because of the technology’s fundamentals, but because ecosystem economics have not been addressed or critical ecosystem players have not come on board. The economic and business model requirements for deployment, as well as a technology’s societal license-to-operate, can and should shape the technical problem definition and development of solutions at all stages of the RDD&D (research, development, demonstration, and deployment) continuum.

To describe adoption risks, the Office of Technology Transitions (OTT) has developed the Adoption Readiness Level (ARL) framework to complement TRL, and provided an assessment tool on the U.S. Department of Energy’s (DOE) website. It’s a very thorough picture of new technology adoption.

Also, another great resource from DOE is the Liftoff Reports. DOE’s Pathways to Commercial Liftoff reports provide public and private sector capital allocators with a perspective as to how and when various technologies could reach full-scale commercial adoption– including a common analytical fact base and critical signposts for investment decisions. The first Liftoff Reports are focused on advanced nuclear, carbon management, clean hydrogen, and long duration energy storage, Virtual Power Plant, Industrial Decarbonization.

Recommended resources:

Activate: Techonomics: Establishing best practices in early-stage technology modeling

Department of Energy: Techno-economic, Energy & Carbon Heuristic Tool for Early-Stage Technologies

Climate tech companies just had their best quarter for fundraising in almost two years, drawing $16.6 billion. Venture capital investment into climate tech is doubling YoY, but the funding gap is not closing fast enough.The first question about investing in climate tech comes into mind – Is this category a capital-intensive play? So, many investors choose only climate software. Actually, there are many variables in answering that question.

One of questions we’ll ask startups is – what’s your capitalization plan? It will impact life or death, speed of growth, capital efficiency for startups, and returns for investors. There are strategies for partnerships and business models to consider for a less capital-intensive growth path. And, when to exit and how? In this panel, we like to cover capitalization and financing strategies in different stages for climate tech startups.

About ClimateTech Investor Panels – This is for accredited private equity angel investors, venture capitalists, and corporate/institutional investors to share insights and investment opportunities and catalyze collaboration to help ClimateTech startups.

Speakers

Paul Burgon, Co-chair of Keiretsu Forum CleanTech Committee, GP of Exit Ventures – Paul is a dynamic operations and investment executive who has invested over $3 billion in almost 100 different companies at high rates of return. Paul balances 1) strategic analysis and strategy development, 2) creating and implementing processes that map to company strategy and 3) team leadership, consistent execution and continuous improvement to create outstanding results.

Karen Sheffield, Finance Director at Visa, Founder & Managing Partner of Pachamama Ventures – Karen is a managing partner of a venture capital firm investing in US early-stage climate tech companies. She is also a Finance Director at Visa and has previously worked for PepsiCo and American Airlines. A self-described operator turned investor, Karen began angel investing 3 years ago and, ever since then, has dedicated much of her time to uncovering opportunities in unlikely places. Karen holds a double degree in Finance and Economics from Texas Christian University (TCU) and an MBA from The University of Texas at Austin.

Interviewed by Jessie Chuang, the topics cover 3 major parts:

Funding gaps and sources for ClimateTech startups and projects

Business and partnership models deciding capital intensity & plan

When to exit and how

Takeaways:

Karen:

I grew up in Peru, and in the country, climate impacts a lot of everyday decisions we make, that’s why I am so passionate about climate investments.

Early-stage startups going to build a proof of concept (POC) need to get initial funding from friends and families, angels (several angel groups focusing on climate tech or impact investing), and government grants – there are so many now for climate tech companies, including IRA and more. Talk to grant writers to help you. Getting grants is hard, but getting funding from VCs before POC is even harder. Non-dilutive funding sources such as grants from governments are crucial for early-stage companies. and now more foundations and family offices want to invest in climate startups. Catalytic capital funds emphasize more on impact instead of maximizing financial returns solely. After you have revenue, there are revenue-based financing mechanisms that can help.

I have 15 years of experience working in Fortune 500 companies, I’ve witnessed the interest in building corporate VCs (CVC) growing significantly. Visa and Pepsi all have CVCs. Most CVCs might take a board seat if they invest to guide the startups, they have very broad interests, not limited to their current business lines, and have lots of funding to experiment. The chief sustainability offices (CSO) in large companies want to partner with climate tech innovators and achieve more than ESG compliance. Of course, there are pros and cons to consider when working with CVCs or corporate partners.

Paul:

The best outcomes in climate tech happen when companies can align their development milestones with their capital strategy.

A big difference between the cleantech 1.0 era and now is that the capital stack for climate tech has been developed rapidly and much more mature in the past 5-7 years. There are billions of hardware or cleantech funds, we see CVCs exploding, we see customer-financing models (customers as investors to build win-win outcomes, be creative, and build partnerships with customers), DOE’s loan office can support commercialization stage projects, and there are growth funds and infrastructure funds looking to back hard tech, etc. These didn’t exist 5-7 years ago, all are narrowing funding gaps substantially for first commercial operations. Especially CVCs can become your potential acquirers, so, look at companies in the ecosystem, and build partnerships.

Funding first commercial productions is still the largest funding gap risk. Although not as fast as we like, we do see that large infrastructure funds are coming down and VCs are going up to narrow the gap and reduce the capital intensity of climate tech startups. Also, a lot of innovations aren’t really as capital-heavy as most people imagine.

Paul wrote the following supplementary notes for reference.

Quote from a large climate tech grant writer: Grants are the quintessential way of filling these valleys of death with patient, risk-tolerant, non-dilutive capital. Government grants have historically done a fairly good job in earlier stages with technology risk by supporting R&D. More recently, with the massive flood of public funding into the climate space, there is sufficient funding for the government to put tens and even hundreds of millions of dollars behind a single project, enabling climate tech companies with high CapEx to undertake the large-scale demonstrations or first-of-a-kind deployments that bridge the commercialization valley of death.

Examples of investors with deep pockets for growth and physical assets are starting to raise and deploy investment vehicles earmarked for climate:

Mega-firms: Mega-shops like Brookfield, TPG, Apollo, KKR, Carlyle, Stonepeak, and Blackstone are also flocking to climate raising tens of billions to finance the net-zero transition.

DOE Title 17 Clean Tech Loan Program:

The Title 17 program can support technologies at each deployment milestone—first-of-a-kind deployments that solve applied engineering challenges; follow-on deployments that establish engineering, procurement, and construction excellence and lower total project costs; substantial scaling of deployment and manufacturing capacity to drive advancement along the learning curve; and education of commercial debt markets to enable broadly available debt financing.

Commercially ready technology has been demonstrated at near commercial-scale under expected process conditions with results supporting the expected performance of the proposed deployment. Performance data from testing at pilot and demonstration scales (confirming at least a Technical Readiness Level 6) must have been performed and be available for review in order to confirm commercial readiness. Applications will be denied if the proposed project is for research, development, or demonstration.

No minimum loan amount. It can usually cover 50-70% of eligible project costs, and loans for up to 30 years. Low interest rates. Check out the criteria here.

Thoughts on how and when to exit:

There’s no perfect answer for when to exit. Some people sell too early and leave a lot of money on the table. There are also many, many stories of startups and boards wanting to hold on and try to go public or sell for a billion dollars, and they end up losing a lot of money or almost everything a few years later due to new competitive technology, the team falling apart, or whatever.

In my opinion, you should consider a few basic things in deciding the right time to sell:

The required return of the founders and the key investors/board. Have they made enough money to justify the time and investment?

What are the technology, market and other risks that could derail the future success of the startup and create a loss scenario? You need to be very honest with yourself on this point, most startup teams are way too optimistic about their near-total invincibility in the next several years. There are always big things that can go wrong, even the unknown factors that aren’t visible today.

Do you have a realistic exit opportunity to pursue in the near to medium term? Is an exit a viable option?

Is the team ready for an exit? Sometimes people factors can preclude a successful exit. The team has to be ready, presentable, and complete.

Is the business ready? Are major customers happy, is the business litigation-free, large problem-free? Are major contracts all renewed, not about to expire? Get due diligence issues cleared up before starting the exit process.

If all of these issues are a go, then I would probably err on the side of exiting sooner rather than waiting of a perfect scenario and perfect valuation. Don’t be greedy, take a win, and stay on with the new owner for a while, maybe a long while, or go to your next big thing in my opinion.

How to exit

How to exit is a completely different podcast. I have an hour podcast on just how to exit. If you are ready to exit, you need great advisors and a board that is very experienced in the tactical best practices of exits.

About Global League

Global League is a vetted network of accredited and professional investors collaborating on We select startups from top seed investors(VCs/angel groups) and build a disciplined process to get collective intelligence for investments and venture building. Collaboration and co-investing are our core strategies to connect silos and help the most impactful ventures.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.